Tracxn, the global market intelligence platform for private company data, today released the UK Mental Health Tech Report 2026. The report analyses the UK mental health technology ecosystem, covering 700+ active companies, $595M in total disclosed equity funding across 232 rounds, and the stage-wise capital trends that have shaped the 2019–2026 period, with a focused examination of the workplace mental health sector, which has raised $217M across 68 rounds and produced three strategic acquisitions to date.

The report documents an ecosystem that has moved through a post-pandemic correction into a more selective phase. Total funding fell from a 2021 peak of $158M to $30M in 2024, before a partial recovery in 2025 driven by a single $35M late-stage close, the first disclosed late-stage amount in the ecosystem since 2021. All three recorded exits are acquisitions. Mental Health Awareness Week 2026, organised by the Mental Health Foundation under the theme of Action, provides the backdrop for a sector where the question is no longer whether capital will enter, but which platforms it will concentrate in.

Capital Is Concentrating, Not Retreating

The 2019–2026 funding cycle tells a maturation story rather than a size story. The 2020–2021 expansion gave way to a structured correction through 2024, with seed-stage funding contracting ~85% from its 2021 peak and total annual funding moderating from $158M in 2021 to $30M in 2024 , consistent with the broader global VC environment.

The selective return visible in 2025 reflects a meaningful shift in conviction rather than volume. Unmind's $35M Series C, the first disclosed late-stage close since 2021 represented 80% of the year's total across 11 rounds, pushing average deal size to ~$4M, the highest since 2020. Capital is returning to a smaller set of scaled platforms, not distributing broadly.

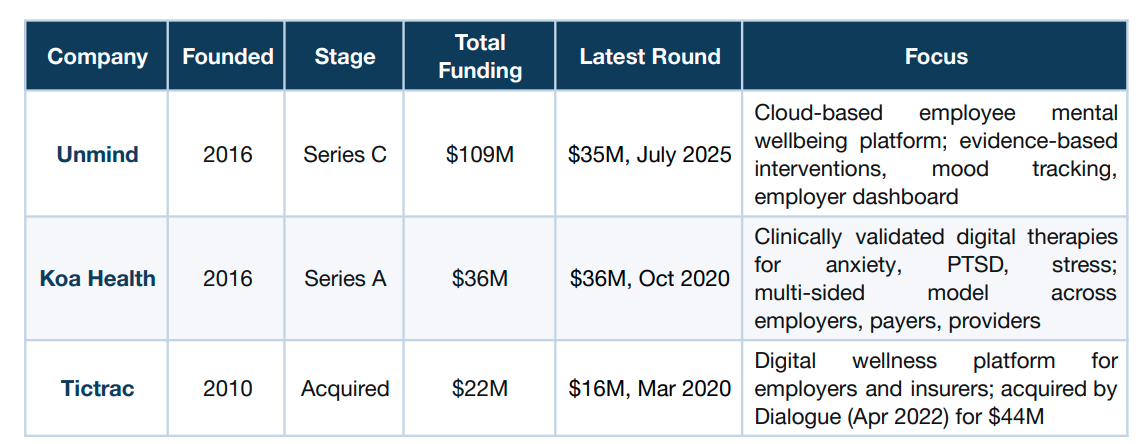

Workplace Mental Health: Where the Capital Is Going

The workplace mental health sector has attracted $217M across 68 rounds, 36% of total ecosystem funding. Capital within the sector is concentrated in three companies — Unmind ($109M), Koa Health ($36M), and Tictrac ($22M), accounting for ~77% of all workplace mental health funding. Each has followed a distinct trajectory: growth-stage scaling, clinical platform development, and strategic acquisition, confirming multiple viable paths exist within the employer-channel model.

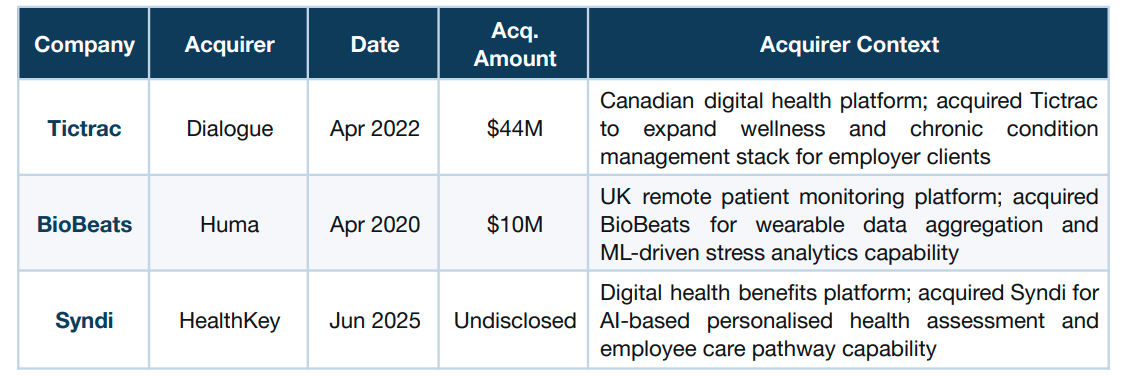

Strategic Acquisitions Define the Path to Liquidity

All three recorded exits - Tictrac ($44M, Dialogue, 2022), BioBeats ($10M, Huma, 2020), and Syndi (HealthKey, June 2025) are strategic acquisitions by health technology and benefits infrastructure platforms. The acquirer profile is consistent: organisations adding validated employer distribution or clinical capability to their stacks, rather than financial sponsors seeking multiple expansion.

The June 2025 Syndi acquisition confirms that acquisition demand has persisted through the funding correction, and Tictrac's $44M exit against $22M raised demonstrates meaningful capital returns are achievable in this sector.

.svg)