Tracxn, the global startup and private company intelligence platform, released The COP29 Impact Report: Tracking UK Climate Capital Flows. The report analyses 155 UK climate-tech funding rounds completed between December 2024 and April 2026, assessing whether the post-COP29 policy cascade translated into measurable capital movement.

The UK was chosen as the primary test case for a specific reason: it is one of the few economies where the full policy-to-capital chain can be traced end to end — with its own carbon market (UK ETS), a state green investment vehicle (the National Wealth Fund), a clean energy mandate with a fixed deadline (Clean Power 2030), and one of Europe's deepest climate-tech VC ecosystems. The report's verdict is calibrated: COP29 reshaped how UK climate capital is allocated, without broadly increasing its volume.

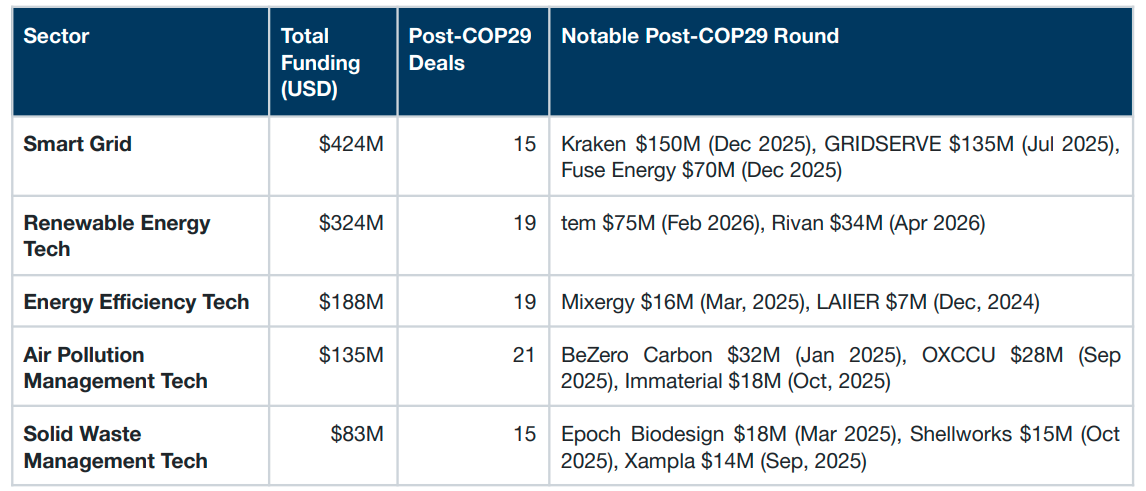

Smart Grid Is Pulling Away — and the Policy Maths Explain Why

Smart Grid attracted more post-COP29 capital than any other sector, with $424M across 15 deals. Three rounds exceeded $50M — Kraken ($150M, December 2025), GRIDSERVE ($135M, July 2025), and Fuse Energy ($70M, December 2025). The sector's outperformance is directly traceable to two converging policy instruments: the Clean Power 2030 mandate, which created structural demand for grid management and storage infrastructure, and the UK-EU ETS linkage announced in May 2025, which strengthened long-term pricing certainty for grid-connected assets.

The ETS linkage, pending ratification, would create the world's largest carbon pricing market by economic value, a signal significant enough to anchor large-round conviction even before implementation is confirmed. While most deal processes were likely initiated before policy announcements formalised, the coincidence of three outsized rounds in a single 17-month window, is not incidental. The Smart Grid data is the clearest evidence in the report that post-COP29 policy moved institutional-scale capital.

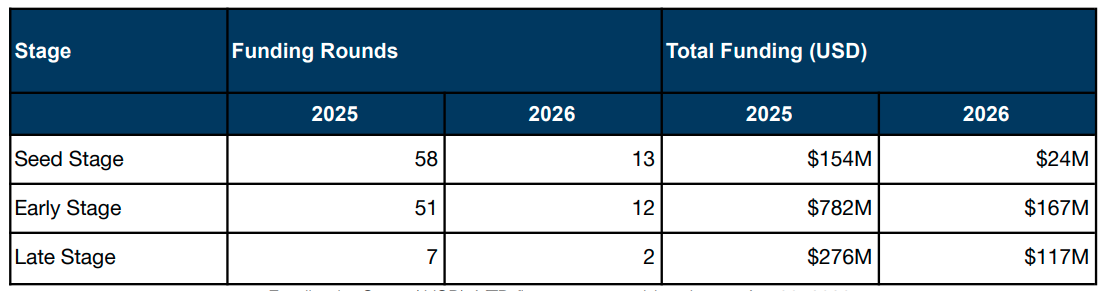

The Pipeline Is Building From the Bottom — and the Top Is Starting to Form

The stage-level data tells a story of healthy ecosystem formation. In 2025, 58 Seed rounds and 51 Early Stage rounds were recorded. This surge in early-stage activity confirms that the post-COP29 policy cascade did widen the venture top-of-funnel, pulling more founders into climate-tech formation. At the Early Stage layer, 51 rounds raised $782M, an average cheque of approximately $15M — consistent with a scaling-phase ecosystem rather than a speculative one.

Late Stage rounds, though fewer in number at 7 deals, pulled in $276M at an average of ~$39M per round — signalling that a cohort of breakout companies is beginning to attract outsized conviction. The 2026 partial-year numbers (13 Seed, 12 Early Stage, 2 Late Stage through April) track consistently with 2025 run-rates, indicating no post-policy cooldown. The formation layer is active, the scaling layer is funded, and the late-stage layer is emerging. The structural question the data cannot yet answer is whether institutional mechanisms can carry this pipeline from scaling to maturity.

Consolidation at the Top: Exit Volume Falls, Deal Value Surges

UK Fintech recorded 22 acquisitions in Q1 2026, down 39% from 36 in Q4 2025 and 27% below the 30 seen in Q1 2025. The quarter's defining exit was Mastercard's acquisition of BVNK for $1.8B in March 2026 - the highest valued transaction of the period by a considerable margin. Founded in London in 2016 and having raised $93.2M in prior funding, BVNK is a crypto-enabled payments infrastructure company whose acquisition signals the extent to which global payment networks are integrating digital asset capabilities into their core operations.

Two further disclosed-price exits reinforced the consolidation theme. Reward, the London-based loyalty platform founded in 2001, was acquired by Rezolve for $230M in February 2026, followed by Admiral Group's acquisition of the commercial insurtech Flock for $109M in the same month. Both exits reflect the ongoing absorption of B2B fintech infrastructure by larger strategic acquirers. No IPOs were recorded in Q1 2026, matching Q4 2025's blank quarter - a signal that the public markets window remains largely closed despite improving private market conditions.

Carbon Markets: Verification Is the New Capture

For years, the UK carbon market investment story was dominated by carbon capture ventures. Post-COP29, that character has changed. The most significant carbon market round in the 18-month window was BeZero Carbon's $32M Series C in January 2025 — a company operating in carbon ratings and MRV (Measurement, Reporting and Verification), the infrastructure layer that Article 6 of the Paris Agreement now requires to function at scale. COP29 advanced the operationalisation of Article 6 standards for both bilateral trading (Article 6.2) and the centralised UN carbon market (Article 6.4), creating commercial viability for verification and accounting infrastructure that didn't previously exist.

The total carbon market deal count remains limited — BeZero Carbon, Origen ($13M, January 2025), and CocoonCarbon ($15M, March 2026) are the named examples in the 17-month window — and the data does not yet support classifying London as a global carbon markets hub. What the data does show is that the pipeline's character has pivoted: investment is moving toward the verification, accounting, and credit infrastructure layers that a functioning Article 6 market demands, rather than toward capture technology alone. This is an early-signal shift that the next COP cycle will either confirm or stall.

.svg)