Tracxn Technologies Limited, a leading data intelligence platform, today released the UK Fintech Quarterly Funding Report - Q1 2026, a comprehensive analysis of funding activity, investor behaviour, exits, and geographic trends across the United Kingdom's financial technology sector.

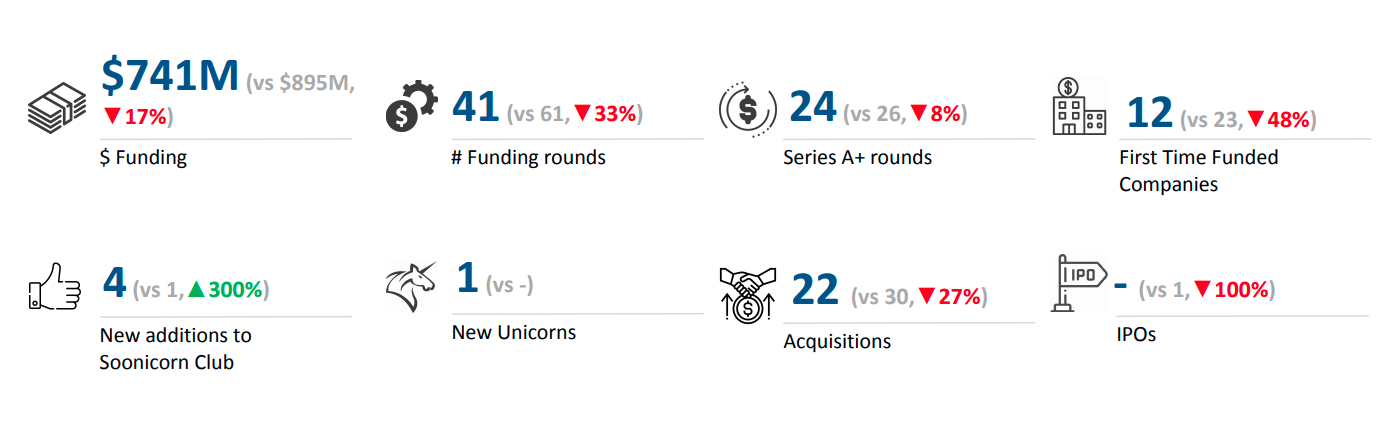

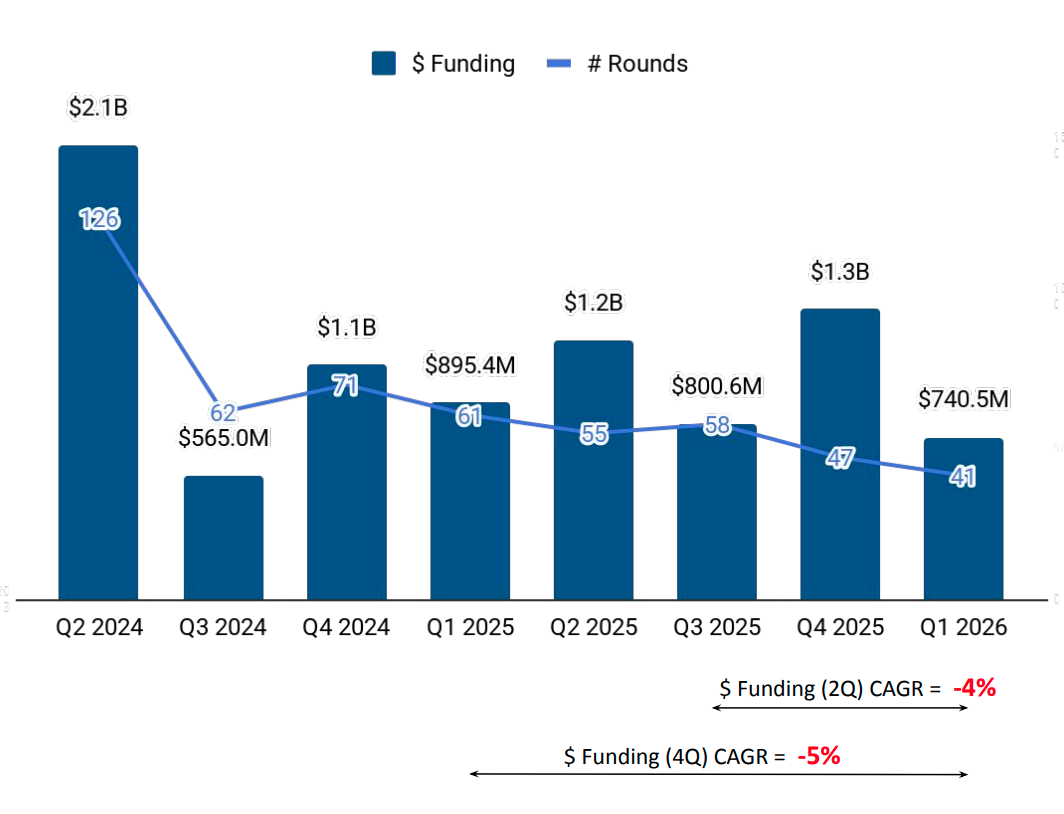

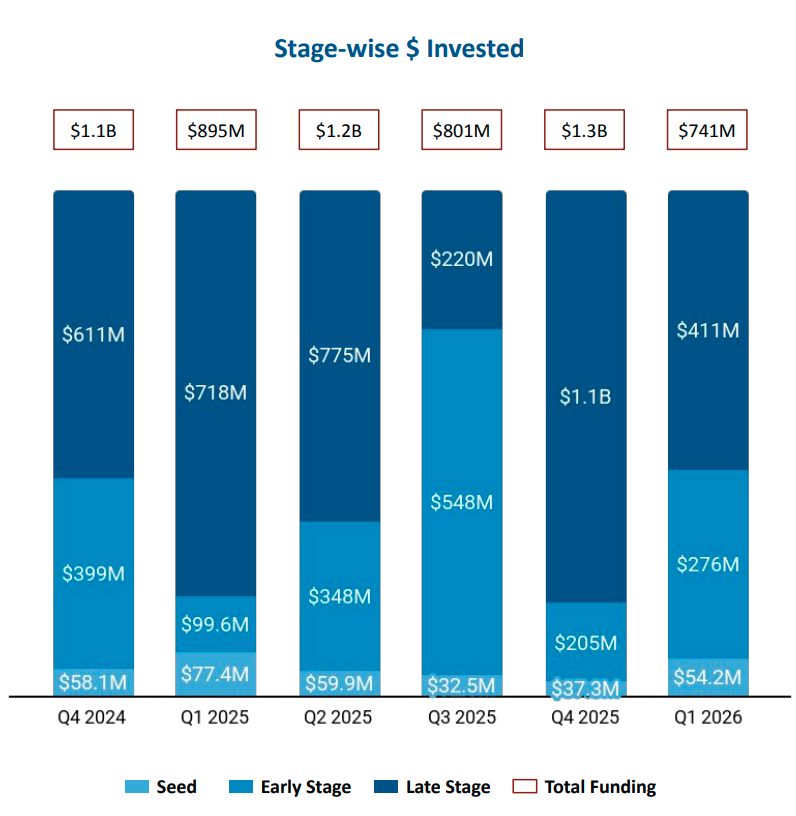

UK Fintech raised $741M across 41 rounds in Q1 2026 - a 43% decline from $1.3B in Q4 2025, yet the quarter's composition tells a different story. Early-stage funding rose 35% vs Q4 2025 and 177% vs Q1 2025, seed funding climbed 46% vs Q4 2025, and four companies joined the Soonicorn Club. Late-stage funding contracted 62% vs Q4 2025 to $411M, driving the aggregate decline - but a closer read suggests investors are repositioning rather than withdrawing.

Early Capital Accelerates as Late-Stage Retreats

The most significant structural shift in Q1 2026 was the divergence across funding stages. Early-stage investment reached $276M - up 35% from $205M in Q4 2025 and 177% above $99.6M in Q1 2025 - even as the overall market declined, underscoring that compression was concentrated at the top of the funding ladder. Late-stage funding bore the full weight of the retreat, falling 62% from $1.1B in Q4 2025 to $411M, with only two rounds exceeding $100M - 9fin Technologies ($170M, Series C) and Allica Bank ($155M, Series D) - while seed funding reached $54.2M, up 46% from $37.3M in Q4 2025, with 41 total rounds reflecting fewer but larger cheques being written across all stages.

Investor activity mirrored this stage-wise divergence. At the seed stage, Fuel Ventures, MMC Ventures, and Founders Factory led deployment, backing early-conviction bets across the ecosystem. SmartFin, Cathay Innovation, and MiddleGame Ventures were the most active at the early stage - with SmartFin notably doubling its investment count vs Q1 2025, participating in both Fimple and incard. At the late stage, TCV, Ventura Capital, and Spark Capital anchored the quarter's largest rounds, with TCV and Ventura Capital backing Allica Bank's unicorn-making Series D and Spark Capital co-leading 9fin Technologies' $170M Series C.

The Deals That Defined Q1: Capital Concentrating in Platform Businesses

The quarter's two headline rounds reflect a clear investor thesis: backing infrastructure-layer fintech businesses with demonstrated scale. 9fin Technologies, the London-based financial data and analytics platform founded in 2016, closed a $170M Series C in March 2026 - backed by Spark Capital, CPP Investments, and Highland Europe. Allica Bank's $155M Series D in February 2026, led by TCV and Ventura Capital, was equally significant: founded in 2017 and focused on SME banking, Allica raised $334M across four prior rounds before claiming Q1 2026's sole formal unicorn designation - a longer, more capital-intensive path shaped by the regulatory demands of building a licensed banking institution.

Beyond the top two rounds, funding concentrated in specific business models. Digital Trading Platforms led all categories with $211M across four rounds, anchored by 9fin Technologies, followed by Digital Banks at $155M from Allica Bank's single round. Crypto Financial Services attracted $59M across three rounds, including Cryptio's $45M Series B, while Insurance Data Software Solutions and Insurance Policy Software rounded out the top five at $50M and $48.6M respectively - a sign that insurtech infrastructure is drawing sustained institutional attention.

Consolidation at the Top: Exit Volume Falls, Deal Value Surges

UK Fintech recorded 22 acquisitions in Q1 2026, down 39% from 36 in Q4 2025 and 27% below the 30 seen in Q1 2025. The quarter's defining exit was Mastercard's acquisition of BVNK for $1.8B in March 2026 - the highest valued transaction of the period by a considerable margin. Founded in London in 2016 and having raised $93.2M in prior funding, BVNK is a crypto-enabled payments infrastructure company whose acquisition signals the extent to which global payment networks are integrating digital asset capabilities into their core operations.

Two further disclosed-price exits reinforced the consolidation theme. Reward, the London-based loyalty platform founded in 2001, was acquired by Rezolve for $230M in February 2026, followed by Admiral Group's acquisition of the commercial insurtech Flock for $109M in the same month. Both exits reflect the ongoing absorption of B2B fintech infrastructure by larger strategic acquirers. No IPOs were recorded in Q1 2026, matching Q4 2025's blank quarter - a signal that the public markets window remains largely closed despite improving private market conditions.

London's Lock on Capital - and the Cities Beginning to Stir

London retained its structural dominance in Q1 2026, accounting for 97% of all UK Fintech funding at $718M - anchored by the quarter's two largest rounds, 9fin Technologies ($170M) and Allica Bank ($155M), both London-based. Yet Q1 2026 introduced notable signals from outside the capital: Belfast registered $12M driven by TeamFeepay's Series A, Cambridge $8M via Theia Insights, Cardiff $1.8M, and Haywards Heath $1M - none of which appeared in Q4 2025's top city rankings, making their simultaneous emergence worth tracking as early evidence that regional fintech ecosystems are beginning to attract their first institutional footholds.

.svg)