Tracxn Technologies Limited, a leading data intelligence platform, today released its Geo Quarterly Report: Maharashtra Tech - Q1 2026, covering all equity funding activity across Maharashtra-based tech companies from January 1 to March 31, 2026.

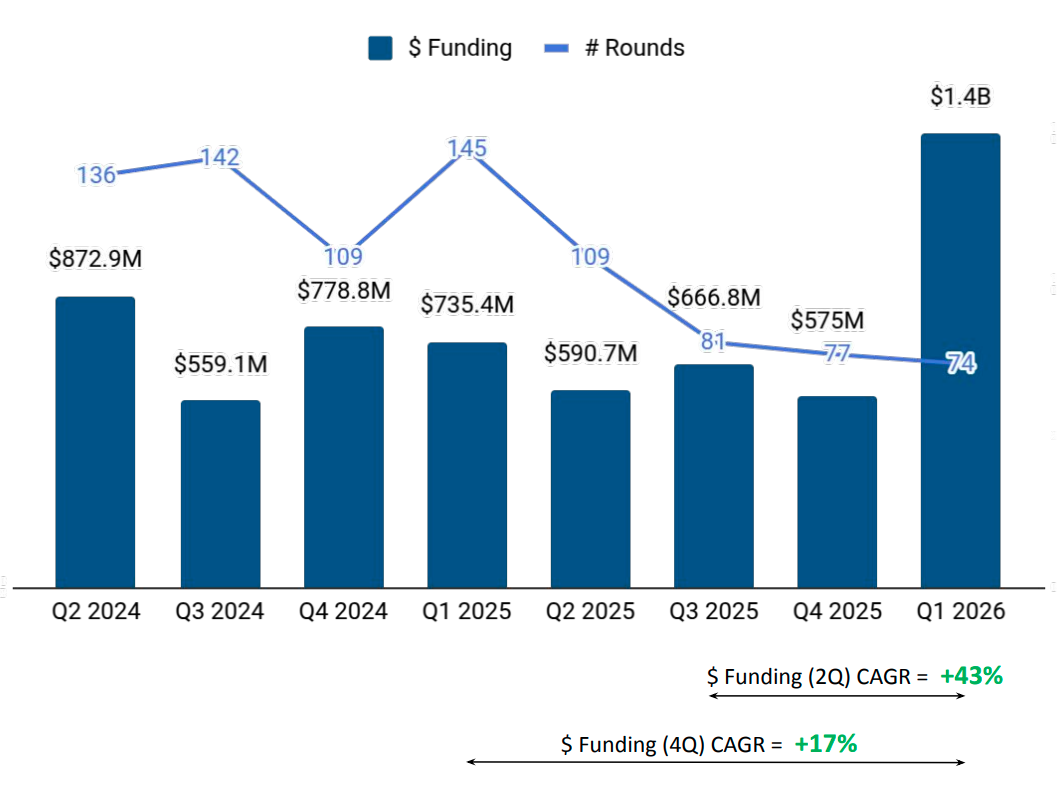

The report finds Maharashtra's tech ecosystem at an inflection point: headline funding reached $1.4B - the highest in eight quarters - even as the number of rounds fell to a two-year low of 74. The dominant theme is concentration: in capital (two companies raised above $100M), in sector (Enterprise Applications alone accounted for 65% of total funding), and in geography (Mumbai's 90% share of state funding was its highest recorded level in recent history).

Capital Is Concentrating, Not Spreading

Q1 2026 closed with $1.4B raised across just 74 rounds - the lowest round count in eight quarters - with Neysa ($600M, Series B) and Weaver ($156M, Unattributed) together accounting for more than half of all capital deployed. GreenCell Mobility ($89M, Series C), Ecofy ($55M, Series B), and Exxat ($45M, Series C) were the next significant rounds. The top business models by funding - IaaS ($600M), Online Lenders ($263M), Public Transit ($104M), and Advanced Solar Energy Generation ($69.7M) - confirm that capital is flowing toward infrastructure and climate-adjacent platforms.

On the investor side, StartupLanes (3 investments), Inflection Point Ventures (2), and Venture Catalysts led Seed Stage activity, while Peak XV Partners, Sixth Sense Ventures, and Unilever Ventures were the most active at the Early Stage. At the Late Stage, Elev8 and Sofina led dealmaking - reflecting a market where institutional conviction is firmly anchored at the growth end of the funding spectrum.

Sector Dominance and the Enterprise AI Overhang

Enterprise Applications, FinTech, and Retail were the three top-performing sectors in Q1 2026. Enterprise Applications commanded $884M - a 395% rise from Q1 2025's $179M - powered almost entirely by Neysa's AI acceleration cloud infrastructure round. FinTech raised $315M across multiple rounds including Weaver's $156M and Knight FinTech's $24M Series A, reflecting sustained institutional interest in alternative lending and digital financial infrastructure. Retail collected $216M, a 20% rise from Q4 2025's $180M, driven by consumer brand and grocery platforms including The Whole Truth Foods ($34M, Series D) and Bonkers Corner ($11M, Series A).

The investor composition behind these sectors reveals a market where capital is flowing with clear intent rather than broad experimentation. Enterprise Applications alone captured 65% of all funding deployed in the quarter, while FinTech and Retail together added another 39% - meaning just three sectors absorbed virtually all of Maharashtra's startup capital in Q1 2026. This level of sector concentration, where the top three account for the overwhelming majority of funding, points to a ecosystem where investors are doubling down on proven categories rather than exploring new ones. With 74 total rounds closed against $1.4B deployed, the implied deal scale signals that the market is rewarding scale and defensibility over early-stage experimentation.

Exits: Selective but Significant

Q1 2026 recorded one IPO and five acquisitions across Maharashtra. Fractal Analytics went public in February 2026 at a market capitalisation of $1.7B, standing as the standout liquidity event of the quarter.

On the acquisition front, Wellbeing Nutrition's $175M deal with USV India was the highest-valued transaction, followed by SILA's acquisition of SMS Integrated Facilities Services at $29.8M. The remaining three deals either carried no disclosed value or closed below $200K, keeping overall acquisition volume modest despite the uptick in deal count from Q1 2025's four transactions.

Geography: Mumbai's Grip Tightens

Mumbai captured 90% of Maharashtra's total funding in Q1 2026, cementing its position as the state's dominant startup hub. Pune followed at 8% ($104M), anchored by Exxat ($45M, Series C), Palmonas ($40M, Series B), and Unbox Robotics ($14M, Series B). Thane contributed $24.3M, while Nashik and Navi Mumbai together accounted for under 1% of state funding - reflecting a funding landscape where capital is concentrated not just by sector and stage, but firmly by geography.

About Tracxn

Tracxn Technologies Ltd. is a data intelligence platform for private market research, tracking 7.5+ million entities through 2900+ feeds categorised across industries, sub-sectors, geographies, and networks globally. It has become one of the leading providers of private company data and ranks among the top five players globally in terms of the number of companies and web domains profiled.

.svg)