Tracxn Technologies Limited, a leading data intelligence platform, today released its Geo Quarterly Report for Europe Tech covering Q1 2026 (January–March 2026). The report tracks funding activity, investor behaviour, exit trends, and city-level dynamics across the European technology ecosystem.

Europe's tech market in Q1 2026 presents a headline of growth masking a story of compression. Total equity funding reached $17B — 6% of global tech funding and the highest quarterly figure in two years — yet the number of rounds declined, unicorn formation hit a multi-year low, and acquisitions contracted sharply. The quarter was shaped by a small number of transformative deals in AI infrastructure, cloud compute, and robotics that accounted for a disproportionate share of capital deployed.

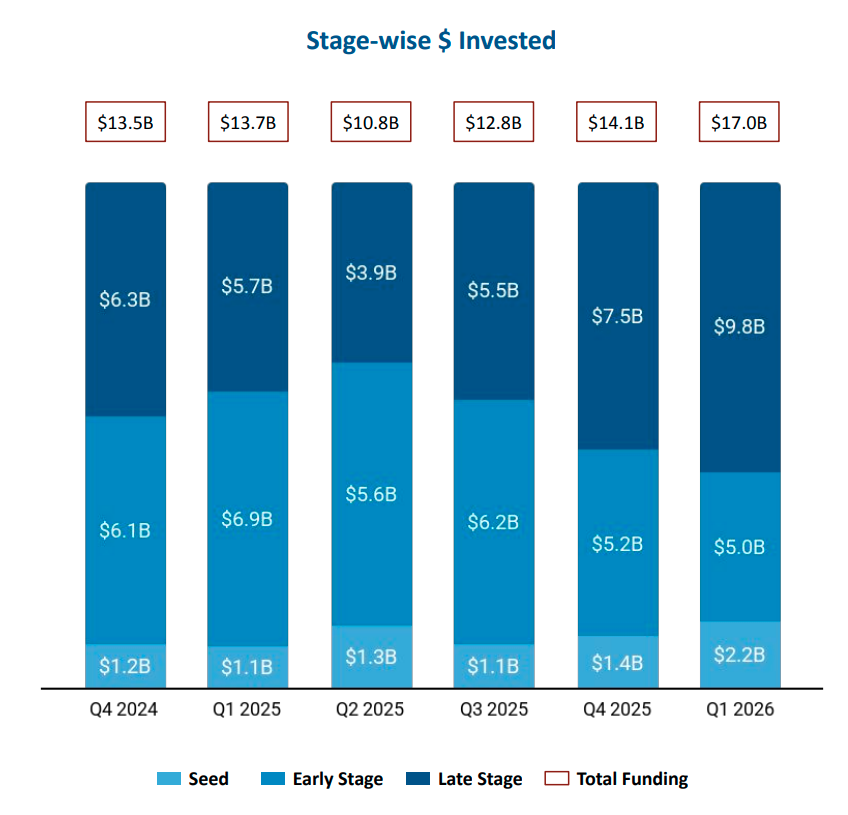

Capital Is Concentrating, Not Retreating

Europe's total tech funding reached $17B in Q1 2026 — its strongest quarterly figure in two years — yet deal count fell 18% versus Q1 2025 to 764 rounds. The divergence is not noise: average deal size expanded materially, and the composition shifted decisively toward late-stage. Late-stage funding reached $9.8B — up 30% from Q4 2025 and up 73% from Q1 2025 — with three deals alone (Nscale's $2B Series C, Neura Robotics' $1.2B Series C, and Wayve's $1.2B Series D) collectively accounting for over $4.4B of that total. The barbell dynamic was equally pronounced at the earliest stage: seed funding rose 95% versus Q1 2025 to $2.2B across 78 rounds. But the early stage contracted 27% versus Q1 2025 to $5B — investors appear willing to make small discovery bets and large conviction bets, while exercising significant restraint in between.

The investor landscape mirrors this concentration dynamic. At the seed stage, Y Combinator, SFC Capital, and HTGF led deployment, reflecting sustained early-stage conviction in European founders. At the early stage, Alstin Capital, Index Ventures, and Invest-NL anchored activity, signalling that established franchises continue to back the continent's most promising growth-stage companies. Late-stage deployment was driven by DST Global, Sapphire Ventures, and Sofina — reinforcing that the largest European rounds continue to attract both global and regional capital, a strong vote of confidence in the quality of assets being built here.

AI Infrastructure and Deep Tech Define the Quarter

The deals that moved Q1 2026's numbers were concentrated in sectors building foundational infrastructure from scratch. AI Infrastructure was the largest funding category at $4.8B; HPC as a Service led all business models at $2.8B through Nscale alone. Autonomous Vehicles drew $1.4B via Wayve; Industrial Robotics $1.3B across seven rounds anchored by Neura Robotics. At the sector level, Enterprise Applications received $12.7B — a 101% increase over both Q4 2025 and Q1 2025 — while Enterprise Infrastructure rose 250% to $3.2B compared to Q1 2025.

FinTech declined 22% versus Q4 2025 and 14% versus Q1 2025 to $1.7B — not because investors retreated, but because no single deal matched the scale of the AI and robotics rounds. The sector remained structurally active, evidenced by Allica Bank's unicorn milestone and the Mastercard–BVNK acquisition at $1.8B. The divergence between FinTech and Enterprise Applications reflects a deliberate reallocation of late-stage capital toward sectors where AI is creating new infrastructure categories rather than incrementally improving existing ones.

Exits Compress as the Bar for Public Markets Rises

Europe recorded just four IPOs in Q1 2026 — down 43% versus Q1 2025 and 50% from eight in Q4 2025. AgomAb Therapeutics listed at a $780M market cap after raising $327M in pre-IPO funding; General Oceans listed at $415M. The quality of exits, however, signals that Europe's public market pipeline is maturing — with companies listing at stronger valuations and greater investor backing than in prior cycles.

Acquisitions fell 37% versus Q1 2025 to 263. The deals that did close were significant in scale: Mastercard's acquisition of BVNK at $1.8B, eBay's re-acquisition of Depop at $1.2B, Genius Sports' purchase of Legend at $1.2B, and Danone's acquisition of Huel at $1.2B. The concentration of marquee deals signals that strategic acquirers remain highly selective but deeply committed — prioritising quality over volume and reinforcing confidence in European tech as a source of category-defining assets.

London Pulls, Paris Holds Firm

London-based companies received $6.7B in Q1 2026 — 39% of all European tech funding, up sharply from 19% in Q4 2025. Nscale, Wayve, FluidStack, ElevenLabs, and Allica Bank drove this concentration. Paris followed with $2B (12%), anchored by AMI Labs' $1B seed round; Metzingen entered the top five with $1.2B entirely attributable to Neura Robotics. London and Paris together commanded over half of all European venture capital deployed in the quarter.

.svg)