Tracxn Technologies Limited, a leading data intelligence platform, today released the Japan Tech Quarterly Funding Report for Q1 2026, covering all equity funding activity in Japan's technology sector from 1 January to 31 March 2026.

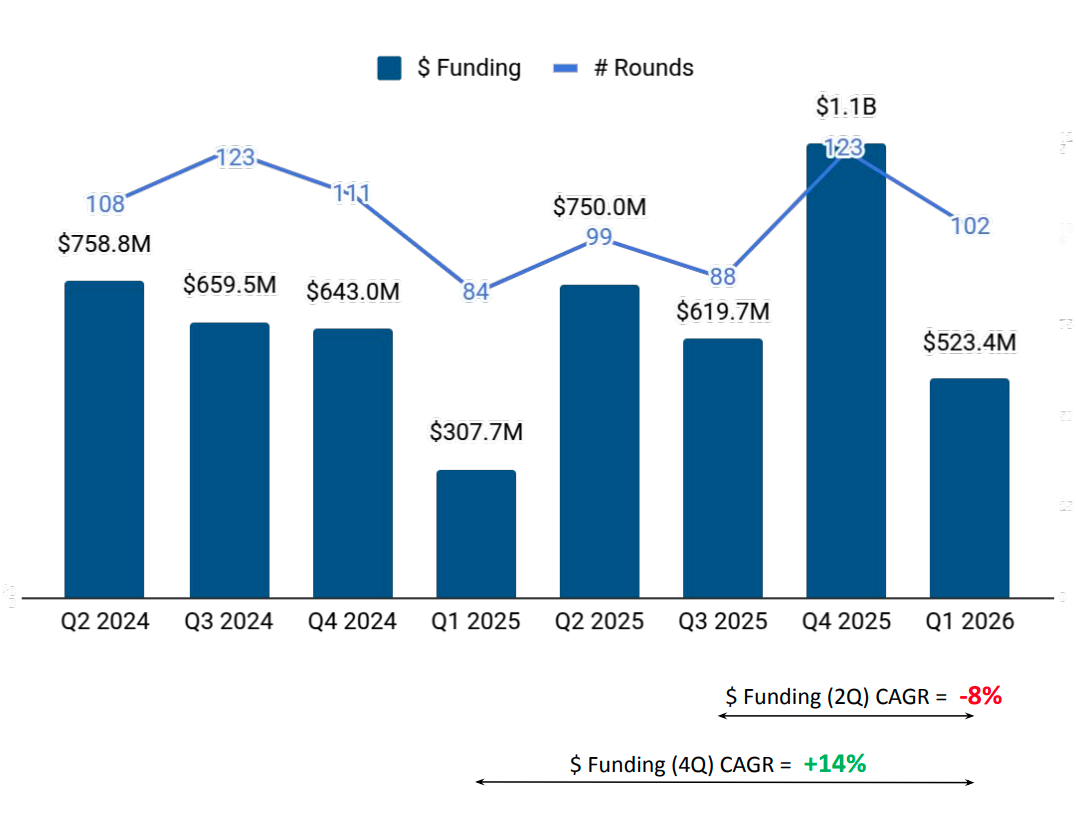

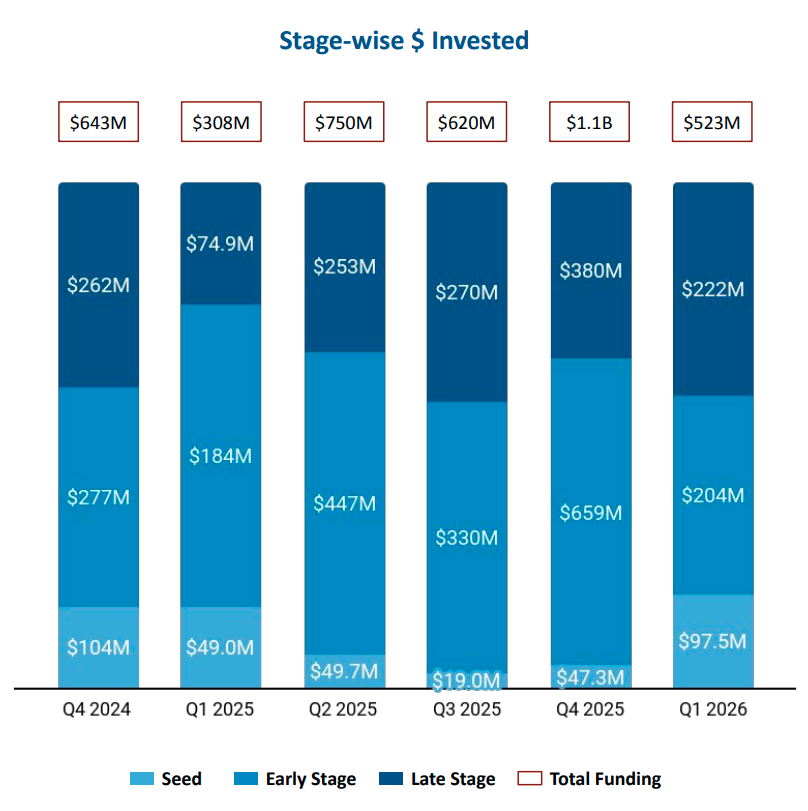

The quarter recorded total funding of $523M across 102 rounds, representing a 70% increase over Q1 2025's $308M even as total activity contracted sharply from the elevated $1.1B deployed in Q4 2025. With no funding rounds exceeding $100M - a threshold breached three times in the prior quarter - capital was distributed more evenly across stages and geographies, with seed funding posting its strongest growth in four quarters and new city clusters outside Tokyo emerging as meaningful contributors.

Capital Is Spreading, Not Concentrating

Q1 2026's defining shift was the disappearance of megadeals - the three $100M-plus rounds that inflated Q4 2025 had no equivalent this quarter, yet deal count fell only modestly from 123 to 102, and rose 21% from Q1 2025's 84, keeping velocity healthy even as average deal size compressed. The clearest beneficiary was seed, where $97.5M in funding more than doubled both Q4 2025 ($47.3M) and Q1 2025 ($49M), pointing to a deliberate investor pivot toward early-stage origination. The quarter's top rounds reflected this distributed-capital theme: Interstellar's $93.3M Series F in Taiki anchored the leaderboard, followed by ai&'s unusually large $50M seed round in Yokohama, Akari's $32.7M Series C, and Solafune's $31.6M Series A - a top four diverse by stage, city, and sector.

At the seed stage, Incubate Fund and One Capital led with four investments each, followed by ANRI with three - collectively backing companies including Helpfeel, Solafune, and NOT A HOTEL. Early-stage activity was anchored by Mitsubishi UFJ Capital, the quarter's most active investor with five deals, while SBI Investment and The Gogin Capital each contributed two. Late-stage deployment was more selective, with JIC Venture Growth Investments, SMBC Venture Capital, and B Dash Ventures each recording a single investment - reflecting greater discipline at the growth end even as late-stage funding amounts recovered sharply from Q1 2025 levels.

Deep Tech and Defense Hold the Growth Line

Enterprise Applications remained the largest sector at $233M but fell 56% from its Q4 2025 peak of $533M, while Aerospace, Maritime and Defense Tech moved in the opposite direction - climbing 47% from $87M in Q4 2025 to $128M, making it the only major sector to grow sequentially. Semiconductors pulled back 59% from Q4 2025 to $45M, yet remains dramatically higher than Q1 2025's $4.1M, reflecting a broader strategic push toward domestic semiconductor capability that venture funding is beginning to follow.

The leading business models within these deep-tech sectors reinforce the same theme. Satellite Launch Vehicles attracted the highest funding of any single business model at $96.7M across just two rounds, driven predominantly by Interstellar's Series F. Machine Learning Deployment followed at $50M - a single high-conviction seed round by ai& - while Environmental Data Analysis ($31.6M, Solafune) and Space Engineering ($19M across two rounds) completed a top four dominated by infrastructure and dual-use technologies, signalling where Japan's deep-tech capital is placing its longest-horizon bets.

Acquisitions Accelerate as a Parallel Exit Route

With IPO windows narrowing to three in Q1 2026 versus six in Q4 2025, acquisitions stepped in as the quarter's dominant exit route. Seven deals represented a 133% jump over Q4 2025's three and a 75% rise over Q1 2025's four - the highest quarterly acquisition count in recent periods. Activity was predominantly domestic: ECPower was acquired by Feedforce Group, atena by Kubell, and Logikura by freee, while Procore (US) acquired Kyoto-based DataGrid - a rare cross-border deal signalling that international buyers are again watching the Japanese market. On the IPO side, PayPay's listing at a $10.7B market cap anchored a lean but high-quality class alongside Innovacell ($290M) and J-Pharma ($80.8M).

The investor exit leaderboard was led by Mitsui Sumitomo Insurance with two exits, followed by a cluster of single-exit investors including Open Network Lab, F-Prime Capital, JIC Venture Growth Investments, Monex Ventures, and Scrum Ventures. The breadth of that list - spanning corporate VCs, institutional investors, and specialist funds - reflects the maturation of Japan's investor base and its growing ability to realise returns across multiple exit pathways simultaneously.

Geography in Motion: Taiki, Chiyoda, and the De-Tokyofication of Capital

Tokyo ranked third in Q1 2026 with 11% of quarterly funding, behind Taiki (18%) and Chiyoda City (11%). Taiki's lead was driven almost entirely by Interstellar's $93.3M Series F, while Chiyoda was anchored by Akari ($32.7M), JPYC ($11.9M), and Spectee ($10M). Yokohama entered the top five on ai&'s $50M seed round alone, and Okinawa appeared for the first time with Solafune's $31.6M Series A - a clear sign that capital is reaching beyond Japan's traditional metropolitan hubs.

.svg)