Tracxn Technologies Limited, a leading data intelligence platform, today released its Geo Quarterly Report - India FinTech Q1 2026. The report finds that India's fintech sector raised $513M in the first quarter of 2026, a marginal 2% increase over Q1 2025 but a 9% decline from the preceding quarter.

Beneath the flat top-line sits a sector quietly reconfiguring itself. Round count fell by more than half year-on-year, first-time cheques dried up, and nearly three-fifths of all capital went to companies headquartered in Mumbai. One business model - Online Lending - absorbed 60% of quarterly funding, while adjacent fintech categories saw only modest activity. The signal is not retreat, but selection: investors are writing bigger cheques into fewer, later-stage companies with demonstrated unit economics.

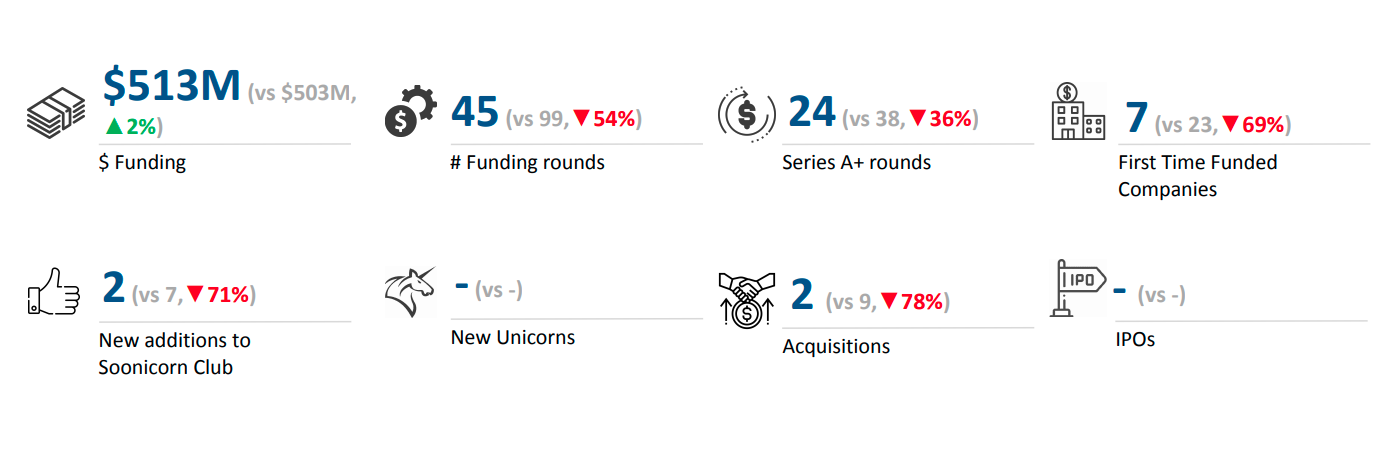

Funding Steady, Deals count reduced

Q1 2026's defining feature is the gap between funding and deal count. Aggregate funding of $513M was nearly flat against Q1 2025's $503M - but round count fell from 99 to 45 over the same period, Series A+ rounds slipped from 38 to 24, and first-time funded companies dropped from 23 to just 7. The same capital is now concentrated across less than half the companies, pointing to a material rise in average cheque size and a far more selective investor stance. Investors are not pulling back from India FinTech - they are concentrating, and the companies that clear the higher bar are walking away with proportionally more.

At seed stage, Fundamentum led with 2 investments, followed by Blume Venture and IIMA Ventures with one each. Early stage saw the most activity - Peak XV Partners and Lightspeed Venture Partners topped the table with 3 investments each, while Accel made 2. Late stage was thinner, with Bessemer Venture Partners backing Innoviti and Analog Capital backing IDfy. On the PE side, Trifecta Capital was the most active with 2 investments, while British International Investment continued its focus on impact-aligned plays through Ecofy and Aerem.

A Barbell Emerges: Late Stage Surges as Seed Contracts

Stage-wise funding tells the story most cleanly. Late-stage rounds drew $273M in Q1 2026, up 126% from $121M in Q4 2025 and 13% higher than Q1 2025. Early stage came in at $214M, down 47% versus Q4 2025 but still up 13% versus Q1 2025. Seed funding, by contrast, fell to $25.7M - down 29% versus Q4 2025 and 65% versus Q1 2025's $72.3M.

The pattern is a classic barbell: capital is accumulating at the ends of the funnel rather than the middle, with the seed end thinning out fastest. Late-stage concentration is being driven by companies that already have scale - Weaver's $156M round, Easy Home Finance's $30M Series C, and Juspay's $28M Series D together account for most of the quarter.

Mumbai Surges Past Bengaluru in Q1 2026

Q1 2026 marks a clear geographic reordering. Mumbai-based firms accounted for 61% of all fintech funding in the quarter at $311M, with Bengaluru trailing at 30% and $152M. Gurugram, Delhi, and Chennai together made up less than 10%. A year ago the picture was reversed - Mumbai held only 9% share in Q1 2025, while Bengaluru commanded 51% of quarterly capital.

The shift tracks the rise of lending and affordable-housing fintech, sectors where Mumbai's proximity to banks, NBFCs, and insurance capital is a structural advantage. Four of the top five Q1 2026 rounds - Weaver, Ecofy, Easy Home Finance, and Idfy - are Mumbai-headquartered. Bengaluru continues to lead in software-layer fintech, with Juspay, Stable Money, Plum, and XFlow among its top-funded names, but the centre of gravity for the largest cheques has clearly moved west.

About Tracxn

Tracxn Technologies Ltd. is a data intelligence platform for private market research, tracking 7.5+ million entities through 2900+ feeds categorised across industries, sub-sectors, geographies, and networks globally. It has become one of the leading providers of private company data and ranks among the top five players globally in terms of the number of companies and web domains profiled.

.svg)