Tracxn, the global market intelligence platform for private company data, today released the Non-Water-Cooled Advanced Reactors Report. The report delivers a comprehensive analysis of the global Fluoride Salt-Cooled (FHR) and Sodium-Cooled Fast Reactor (SFR) ecosystem, covering six companies, three countries, $1.6B in disclosed equity funding, and the regulatory milestones that have defined 2023–2026 as a category-creation period.

The report documents an ecosystem at a structural inflection: two NRC construction permits issued, nuclear-safety concrete poured at Oak Ridge, and the world's most advanced commercial non-LWR reactor advancing toward nuclear island construction in 2026. Three forces, regulatory clearance across independent jurisdictions, hyperscaler offtake commitments, and AI infrastructure capital entering at construction scale have now converged simultaneously for the first time.

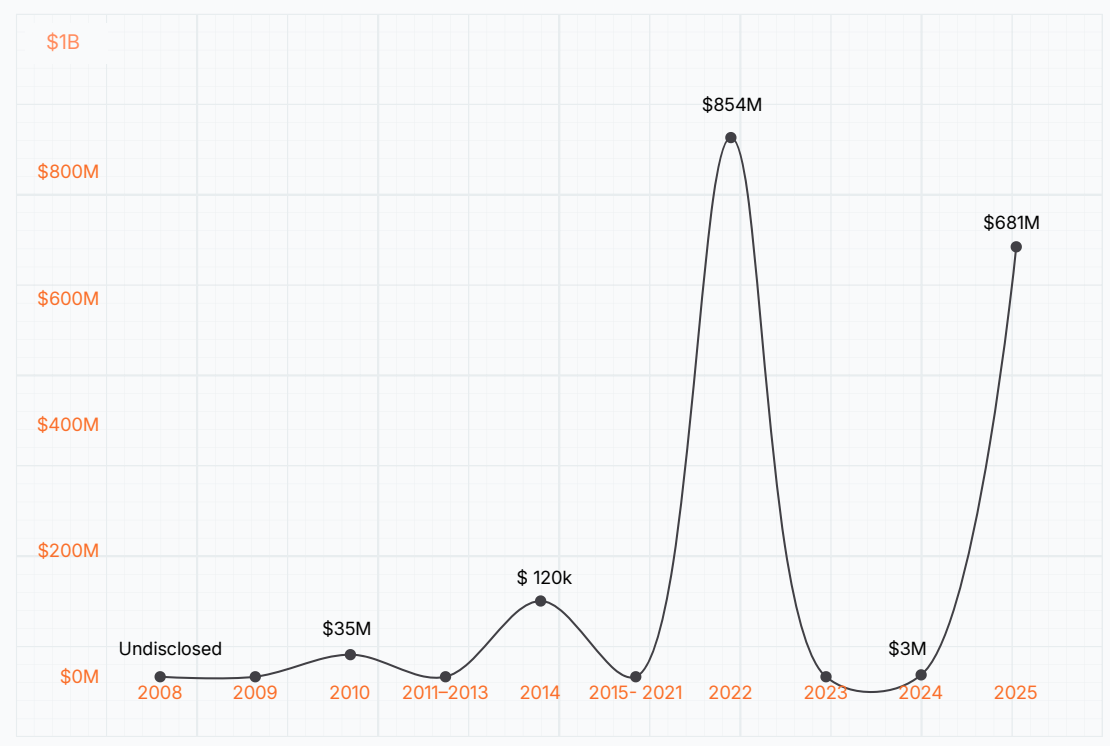

A Silent Year Was the Loudest Signal: The Capital Story

From 2009 through 2021, the ecosystem produced just two disclosed equity rounds. The pattern broke in 2022 with $854M across three rounds, catalysed by the DOE's ARDP framework, which committed federal cost-share that de-risked private investors at a scale. ARDP disbursements themselves sit outside the equity totals in this report. Then 2023 went completely silent, the same year Kairos received its NRC construction permit and TerraPower signed its DOE technology agreement. Capital did not lose confidence; it waited for construction-stage proof and recommitted at ~$681M in 2025.

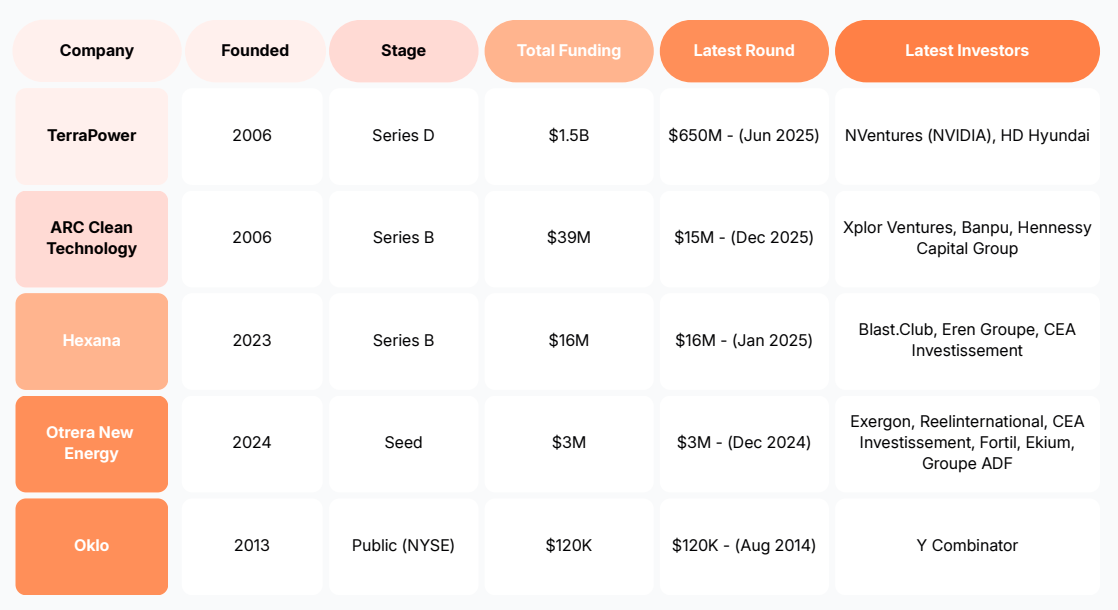

The 2025 wave introduced a new investor archetype: TerraPower's $650M Series D was led by NVentures (NVIDIA), the most significant signal yet that AI compute infrastructure capital is directly backing the energy source its hardware demands. Simultaneously, Hexana ($16M, January) and ARC Clean Technology ($15M, December) joined TerraPower in the same funding year, the first time three or more companies raised equity in the same calendar year, and the first time the European and North American cohorts appeared together in a single funding year. The broadening of the funding curve is the report's most structurally significant 2025 signal.

Three Regulators, Three Countries, 24 Months: The Convergence That Changes the Risk Calculus

Kairos Power's NRC permit in December 2023 was the first non-water-cooled reactor cleared by US regulators in half a century. TerraPower's Natrium permit in early 2026 was the first ever for a commercial non-LWR. ARC's CNSC Phase 2 clearance in July 2025 was the first sodium fast reactor globally to pass that review with no barriers. France's ASNR entered preparatory review for Hexana in 2025.

That concurrence was not coordinated, it reflects three jurisdictions independently concluding the technology is ready. Regulatory uncertainty, long cited as a barrier to capital deployment in advanced nuclear, has visibly declined across all three geographies within the same window. TerraPower's operating license application, the next major regulatory gate for the world's most advanced commercial non-LWR project, will set the global benchmark for non-LWR commercial licensing when filed.

The Exit Architecture and Why Acquisitions Are Still Years Away

One IPO: Oklo's NYSE SPAC listing in May 2024. No acquisitions. Strategic acquirers are yet to move—in nuclear, acquisition valuations are typically tied to operating license achievement, and none of the six companies has an operating reactor yet. That is a couple of years away.

Oklo's NYSE listing - no revenue, 13.2 GW in disclosed framework agreements with Meta and Switch-is the only real-time SFR price signal in the market. It confirms hyperscalers will contract ahead of first operations. These companies are currently priced at construction-stage risk. When operating licenses are achieved, valuations are expected to re-rate significantly, that transition is among the largest valuation jumps in the nuclear asset class.

.svg)