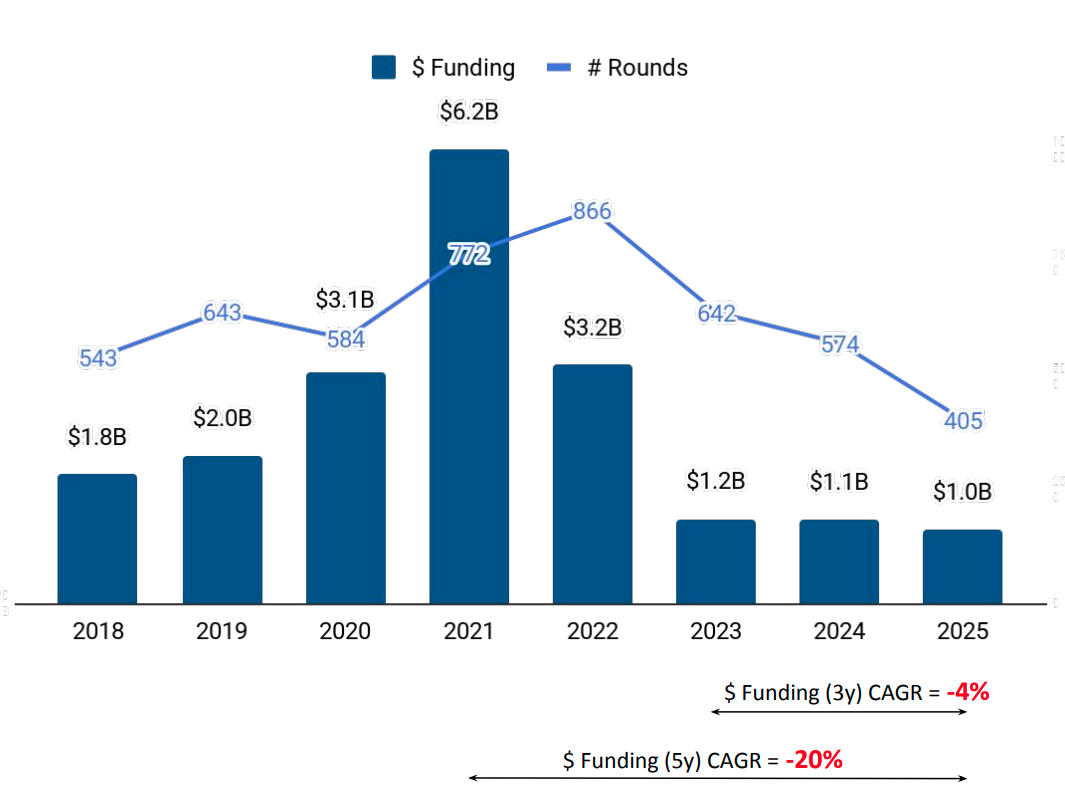

● Funding stabilized at $1B in 2025, representing a marginal 12% year-on-year contraction, while deal volume declined sharply by 29%, signaling a structural shift toward conviction-driven investment and capital discipline over broad-based deployment.

● Early-stage funding demonstrated strong institutional focus, increasing 12% year-over-year to reach $533M even as transaction volume compressed, reflecting investor preference for scaling assets with proven product-market fit and revenue visibility.

● Capital concentration heavily favored established hubs, with Bengaluru securing a dominant $384M, representing 38% of the total market share, followed by Mumbai at $112M, as funding was primarily directed toward globally scalable fintech, deep-tech, and established D2C platforms.

● Driven by strategic consolidation, acquisitions surged 175% year-over-year to 33 deals. The trend was spotlighted by Diginex’s massive $2B takeover of Resulticks, underscoring the immense value locked in enterprise tech platforms.

● The 2025 IPO landscape delivered defining milestones through the public debuts of Lenskart and Zappfresh. With two listings during the year, IPO activity remained relatively measured, and both listings highlight the continued presence of digital-first consumer brands in the public markets.

Tracxn has released its “Women Co-Founders in India Tech – Annual Funding Report - 2025”, highlighting key trends in funding activity, sector performance, deal flow, and investor participation across the ecosystem. The report tracks movements in total equity funding, as well as exits, acquisitions addition, and overall capital deployment within India’s women co-founded technology landscape during the year.

In 2025, India Tech’s women co-founded startup ecosystem secured $1B in funding, down from $1.1B in 2024, marking a 12% year-over-year decline. Deal activity also fell significantly, with the number of funding rounds dropping 29% from 574 in 2024 to 405 in 2025, reflecting a contraction in overall transaction volume.

Seed-stage funding declined from $342M across 456 rounds in 2024 to $261M across 311rounds in 2025, marking a 24% year-over-year decrease and continuing the moderation from the $478M peak recorded in 2022. In contrast, early-stage funding increased from $478M in 2024 to $533M in 2025, reflecting a 12% year-over-year rise, even as deal volume declined from 93 to 79 rounds. Meanwhile, late-stage funding fell from $326M across 25 rounds in 2024 to $213M across 15 rounds in 2025, representing a 35% year-over-year decline.

India recorded two IPOs in 2025, down from three in 2024, reflecting a 33% year-over-year decline in public listings. The year’s IPO activity was driven by Lenskart and Zappfresh, which together accounted for both listings during the period.

India Tech’s women co-founded startup ecosystem recorded 33 acquisitions in 2025, compared to 12 in 2024, marking a significant rise in exit activity during the year. Among the disclosed transactions, Resulticks stood out with a $2B acquisition, followed by Ecom Express at $165M and PeopleStrong at $130M, taking the combined disclosed deal value to $2.3B.

Bengaluru emerged as the top-funded city in 2025, raising $384M and accounting for 38% of the total $1B funding during the year. Mumbai ranked second, securing $112M, which represented 11% of the overall capital raised within India Tech’s women co-founded startup ecosystem.

Investor participation differed across funding stages within India Tech’s women co-founded startup ecosystem in 2025. At the seed stage, Venture Catalysts, Inflection Point Ventures, and Antler emerged as the most active VC investors. Early-stage funding activity was led by Elevation Capital, Vertex Ventures, and Peak XV Partners, while late-stage participation included Creaegis, which was the most active investor during the year.

The India Tech women co-founded ecosystem recorded a year-over-year decline in overall funding in 2025, alongside a notable drop in deal activity. Seed and late-stage investments moderated during the year, while early-stage funding registered growth. The ecosystem witnessed a sharp rise in acquisition activity compared to the previous year, and two public listings. Median deal sizes increased, and total funding levels remained broadly stable for the second consecutive year, indicating concentrated capital deployment within the ecosystem.

.svg)