Tracxn, the global market intelligence platform for private company data, today released Histotripsy: Cutting Without a Blade, a comprehensive analysis of the global histotripsy ecosystem covering all five companies, 14 funding rounds, and the category's only exit to date.

The report documents a medtech category at an inflection point: a new FDA device class created in October 2023, a category leader acquired at $2.3B within 22 months of clearance, and four pre-exit challengers in the US, Canada, and Japan still priced at early-stage valuations. Three structural factors, regulatory clearance, CMS reimbursement assignment, and a proven exit multiple have now converged simultaneously for the first time.

A Mechanism That Is the Moat

Histotripsy fires focused ultrasound pulses into a defined internal target, generating cavitation microbubbles that mechanically liquefy tissue, no heat, no incisions, no radiation. Unlike HIFU and RFA, it is immune to the heat-sink effect, opening a large share of liver, pancreatic, and renal tumours adjacent to major vessels that thermal modalities cannot treat. Each new indication requires a separate FDA clearance, compounding the regulatory moat with every approval.

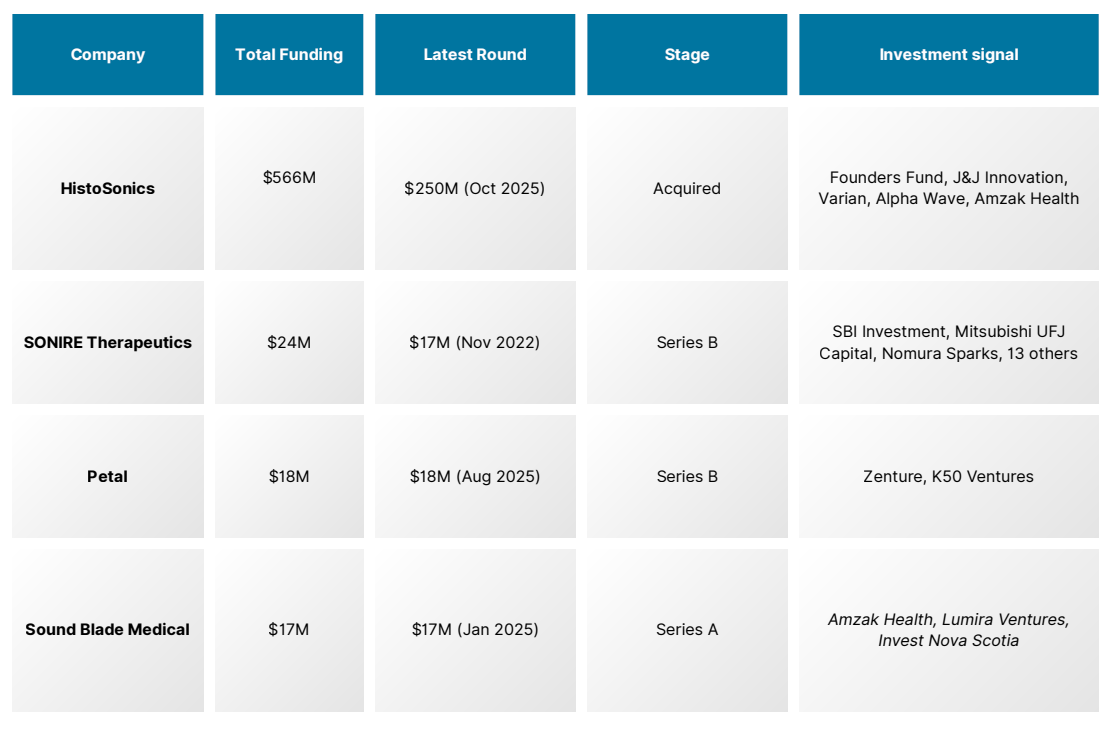

Capital Is Two-Speed: One Giant, Four Challengers at Pre-Strategic Pricing

HistoSonics accounts for $566M of the ecosystem's $625M total, a 90% concentration ratio. Its $250M Series E in October 2025, led by Founders Fund, is the largest single round in histotripsy history. The challenger cohort, SONIRE ($24M), Petal ($18M), and Sound Blade Medical ($17M) have collectively raised less than a quarter of that one round.

The asymmetry is the investment signal, not a flaw. HistoSonics exited with FDA clearance, 2,000+ patients treated, a CMS reimbursement code at $17,500 per procedure, and a 14-year evidence base. None of the challengers hold any of these. Each de-risking milestone they achieve — first clearance, first pivotal readout, first CPT upgrade compresses the gap between current early-stage pricing and eventual strategic acquisition value.

The Companies Building the Next Wave

SONIRE Therapeutics (Tokyo) is the only company targeting pancreatic cancer specifically, running a Phase 2 RCT in Japan while preparing a US IND submission; it holds the only non-US FDA Breakthrough Device Designation in the space. Petal (Los Angeles) is building an AI- and robotics-integrated acoustic sculpting platform, backed by Dr. Fred Moll, co-founder of Intuitive Surgical, explicitly positioning it as a new surgical category.

Sound Blade Medical (Halifax) is developing the only handheld histotripsy system in the ecosystem, designed for endoscopy suites and low-resource settings where HistoSonics' fixed Edison system cannot reach. Arrayus (Burlington, Ontario), still pre-institutional, has a Health Canada approval for uterine fibroids, active cancer trials, and a partnership with Bracco Imaging, at pre-institutional pricing that closes with the first term sheet.

Five Signals That Will Define the Next 24 Months

HistoSonics' HOPE4KIDNEY FDA submission is expected in 2026; approval would expand the cleared indication to kidney tumours and reinforce the multi-indication platform thesis. SONIRE's Phase 2 readout in Japan is the critical non-US proof point — a positive result enables the PMDA pathway, accelerates US plans, and positions SONIRE as an acquisition target for any strategic wanting a non-liver pipeline.

A CPT upgrade from Category III to Category I would unlock broad private payer coverage and materially accelerate hospital adoption — the single largest commercial inflection point in the near term. Entry of additional cross-portfolio institutional investors would signal category-level investing has begun, a pattern that historically precedes M&A consolidation by 18 to 24 months. Medtronic, J&J, Boston Scientific, and Stryker have not yet moved.

.svg)