Tracxn has released its latest report, Startup Growth Beyond India’s Key Startup Hubs: An Ecosystem Snapshot, offering a data-driven analysis of entrepreneurial activity, funding trends, investor participation, unicorn emergence, and exit outcomes across India’s emerging regional startup ecosystems.

As of December 2025, more than 68k startups are headquartered outside India’s primary startup hubs, including Bengaluru, Delhi–Gurugram–Noida, Mumbai–Navi Mumbai–Thane, Hyderabad–Secunderabad, Chennai, Pune, Ahmedabad, and Kolkata. While startup formation has expanded geographically, scale outcomes remain uneven, with funding and exits concentrated within a relatively small number of companies and cities.

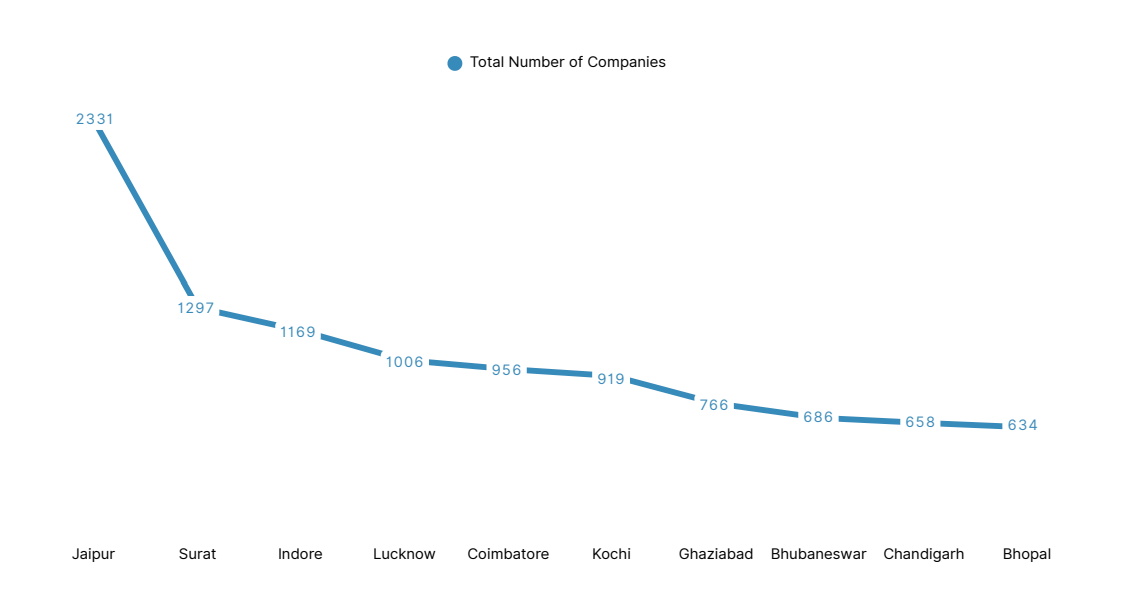

Startup formation beyond the major hubs continues to exhibit strong clustering dynamics rather than uniform national dispersion. Cities such as Jaipur, Surat, Indore, Coimbatore, Kochi, and Lucknow account for a disproportionate share of venture creation, indicating that ecosystem growth is being driven by the deepening of a few regional nodes rather than widespread diffusion across all urban markets. Sectoral activity in these ecosystems remains largely demand-led, with strong representation in EdTech, Internet First Media, Fashion Tech, and Online Grocery platforms. These sectors align closely with regional consumption patterns, industrial strengths, and relatively lower capital intensity compared with enterprise software and deep-technology ventures that typically dominate larger startup hubs.

Funding participation has also matured over the past decade, even as capital deployment remains structurally concentrated. Between 2016 and 2025, startups beyond the key hubs recorded ~2.2K funding rounds and attracted approximately $3.2B in investment. Funding activity peaked during the 2021–2022 venture upcycle before moderating in subsequent years, reflecting broader global capital cycle dynamics. Over time, median round sizes have increased significantly, signalling a transition toward conviction-led investment strategies. Investors are increasingly backing fewer startups with stronger execution visibility, resulting in a funding environment characterised by rising capital depth alongside narrowing participation.

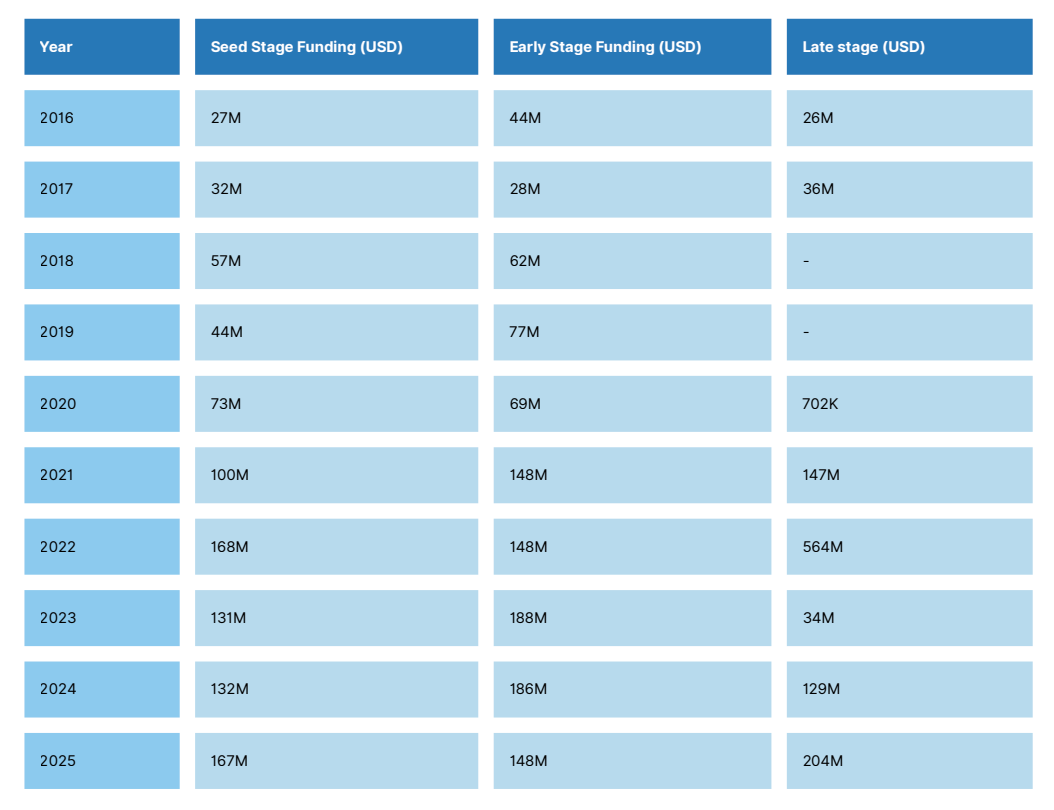

Stage-wise trends reinforce this evolution with clear divergence in capital depth across the funding lifecycle. Seed funding expanded from $27M in 2016 to $167M in 2025, underscoring the role of emerging ecosystems as consistent startup formation engines. However, progression into scale capital remains uneven. Early-stage funding, while structurally higher than pre-2020 levels, moderated from a peak of $188M in 2023 to $148M in 2025, indicating continued friction in the transition from validation to growth. Late-stage deployments remain particularly episodic and concentrated. Late-stage funding surged to $564M in 2022, driven by a small number of large rounds, before declining sharply to $34M in 2023 and recovering to $204M in 2025. This volatility highlights that while billion-dollar outcomes are achievable, building a broad, repeatable pipeline of scale-stage companies beyond primary venture capital centres remains an ongoing structural challenge.

This concentration becomes more visible when examining the largest funding outcomes. The Top 10 funding rounds beyond Key Startup Hubs account for nearly $1B in capital, with companies such as Meril and DeHaat attracting a significant share of growth investment. Mega rounds exceeding $100M remain rare but strategically important, demonstrating that geography is no longer a binding constraint for execution-ready platforms capable of operating at national or global scale. At the same time, the limited frequency of such transactions suggests that large capital outcomes continue to function as proof points of ecosystem progress rather than indicators of systemic parity with India’s primary startup hubs.

Investor participation across these emerging ecosystems remains strongly oriented toward early-stage enablement. Angel networks and seed-focused venture platforms, including We Founder Circle, Venture Catalysts, IIMA Ventures, Inflection Point Ventures, and SucSEED Indovation, play a central role in supporting founder validation and pipeline formation. Typical cheque sizes range from approximately $230K to $3M, reflecting a milestone-driven funding architecture focused on product development, market testing, and capability building. While this has strengthened startup density and experimentation, the relatively limited presence of large growth funds continues to influence the pace at which companies scale.

Unicorn creation and exit activity further illustrate the selective nature of ecosystem maturity beyond major hubs. As of early 2026, only two startups headquartered outside the primary clusters, CarDekho and Molbio Diagnostics have achieved unicorn status. These companies demonstrate that large-scale outcomes can emerge from regional ecosystems, often through longer and more capital-efficient growth trajectories. Exit activity has also progressed gradually, with 102 acquisitions and 33 IPOs recorded between 2016 and 2025. Acquisitions remain the dominant liquidity pathway, while IPO participation is increasing but continues to be concentrated among a relatively small group of operationally mature companies.

Overall, the report concludes that startup ecosystems beyond India’s Key Startup Hubs have transitioned from a phase of early experimentation toward selective ecosystem maturation. While startup formation remains robust and geographically diversified, the next stage of development will depend less on expanding company counts and more on strengthening mid-stage funding pathways, talent networks, and institutional support systems. As regional clusters such as Jaipur, Indore, Kochi, and Surat continue to evolve, they are expected to play an increasingly important role in shaping India’s broader innovation landscape, contributing ecosystem breadth, resilience, and occasional breakout success stories, even as primary startup hubs retain structural advantages in capital access and scale velocity.

.svg)