● India hosts 1,700+ AI-native companies, which have collectively raised approximately $5.5B in equity funding.

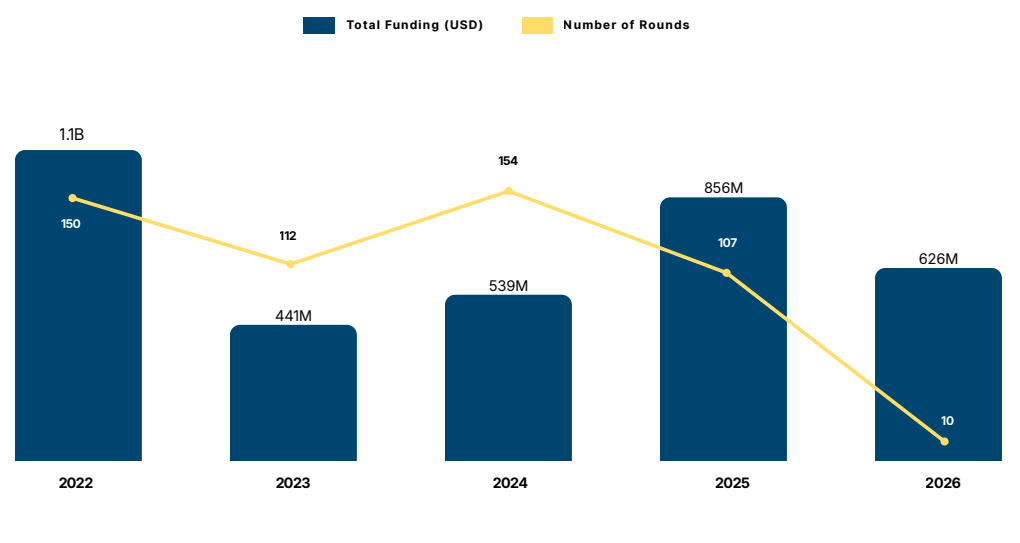

● AI funding in India hit a high of $1.1B in 2022, eased over the following two years, rebounded to $856M in 2025, and has already reached $626M in 2026 YTD.

● The ₹10,372 Cr IndiaAI Mission has allocated GPU compute to 12 foundational model developers, significantly lowering the capital barriers to large-scale domestic model training.

● Domestic model development now spans 2.9B to 105B parameters, supported by structured public–private compute coordination — signaling early but tangible expansion of India’s foundational model capacity

● Global AI funding exceeds $473B, with OpenAI, Anthropic, and xAI collectively accounting for an estimated ~$170B (~36%) of total capital — underscoring the capital intensity and concentration defining frontier AI development globally.

Tracxn has released its latest report, India and the Sovereign AI Shift, offering a data-driven analysis of India’s evolving sovereign AI positioning across foundational model development, infrastructure build-out, capital formation, and digital public infrastructure.

In a multipolar geopolitical environment, control over advanced technologies has become central to economic resilience and national security. Artificial Intelligence sits at the intersection of compute infrastructure, semiconductor supply chains, data governance, and cloud ecosystems. Sovereign AI refers to a country’s ability to develop, govern, and deploy AI systems within its own regulatory and economic framework while remaining globally integrated.

As of 2026, India’s AI ecosystem comprises over 1,700 AI-native companies that have collectively raised approximately $5.5B in equity funding. The ecosystem spans enterprise AI, vertical applications, consumer platforms, and infrastructure layers — reflecting sustained entrepreneurial expansion rather than a short-term generative AI surge.

A structural shift is underway. Earlier phases of India’s AI growth were largely application-led and built atop globally available models and foreign-controlled infrastructure. Today, policy initiatives such as the ₹10,372 Cr IndiaAI Mission, domestic GPU provisioning, semiconductor incentives, and expanding data centre capacity signal deeper participation across upstream layers of the AI stack.

Under the IndiaAI Mission, twelve companies building foundational and specialized models have received structured GPU allocation. Public disclosures indicate domestic model development spanning 2.9B to 105B parameters, including mixture-of-experts architectures optimized for inference efficiency. Sarvam AI, for example, has received allocation of 4,096 NVIDIA H100 GPUs supported by approximately ₹99 crore in compute subsidies. These efforts mark early but measurable expansion of India’s foundational model layer.

Capital formation reflects a multi-year scaling cycle. AI funding peaked at $1.1B in 2022, moderated during 2023–24 in line with broader global venture normalization, rebounded to $856M in 2025, and has already reached $626M in 2026 YTD. Infrastructure-oriented rounds are becoming increasingly visible, highlighted by Neysa AI’s $600M raise at a ~$1.4B enterprise valuation. This signals growing institutional confidence in AI cloud and GPU-backed infrastructure as a scalable asset class.

Globally, cumulative AI funding exceeds approximately $473B, with a significant share concentrated among a small group of frontier model developers. In contrast, India’s capital base remains smaller in absolute terms but more distributed across firms rather than consolidated within a limited set of hyperscale labs.

India’s sovereign AI positioning is anchored not only in capital formation but in deployment depth. The country has one of the world’s largest digitally active user bases and operates population-scale digital public infrastructure platforms such as Aadhaar, UPI, DigiLocker, ONDC, and Bhashini. These programmable rails generate structured digital interactions across identity, payments, commerce, and language services, creating real-world environments for AI deployment at national scale. Global AI laboratories and hyperscale providers have increasingly localized infrastructure commitments in response to this deployment density. Investments such as Google–Adani’s $15B data centre partnership and AWS’s $8.4B infrastructure commitment underscore how India’s user scale is driving compute localization. India’s sovereign AI trajectory is therefore neither isolationist nor purely consumption-driven. It reflects a hybrid model built around scaled digital deployment, incremental infrastructure deepening, and coordinated public–private capacity formation. Domestic training cycles are underway, compute allocation is expanding, infrastructure capital is scaling, and digital public rails provide a uniquely structured deployment base.

The transition remains evolutionary rather than abrupt. Infrastructure depth continues to expand, and foundational model ecosystems remain in active build phase. The question is not whether India will participate in the global AI economy, but how deeply it internalizes critical layers of the intelligence stack over the coming cycle.

.svg)