Tracxn Technologies Limited, a leading data intelligence platform, today released the Geo Quarterly Report: Australia Tech — Q1 2026. The report covers equity funding, investor activity, acquisitions, IPOs, and ecosystem signals for the Australian technology sector from January to March 2026.

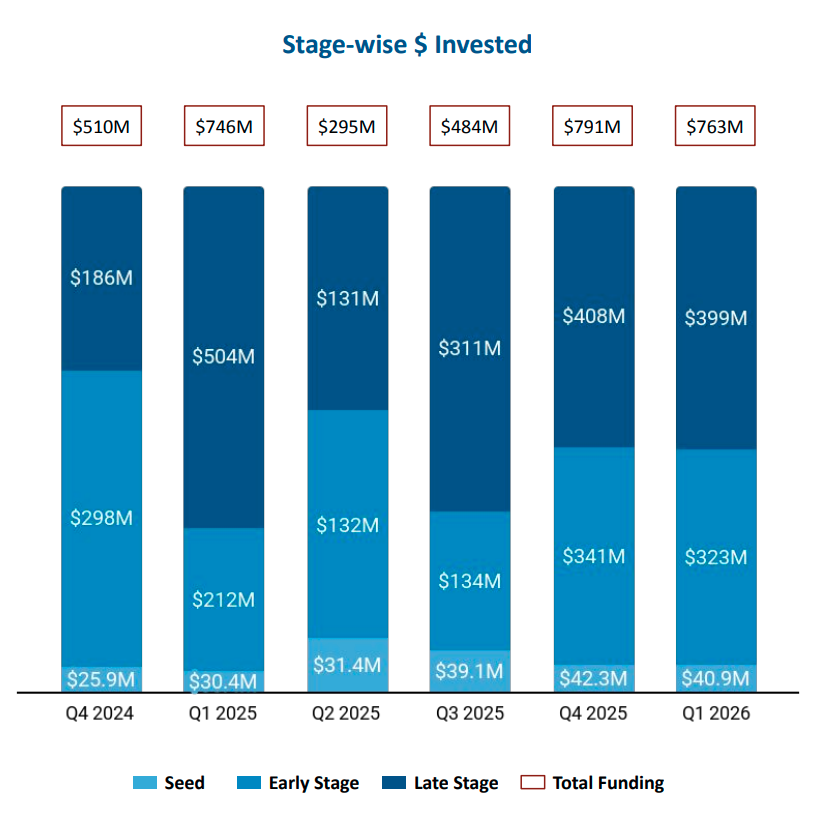

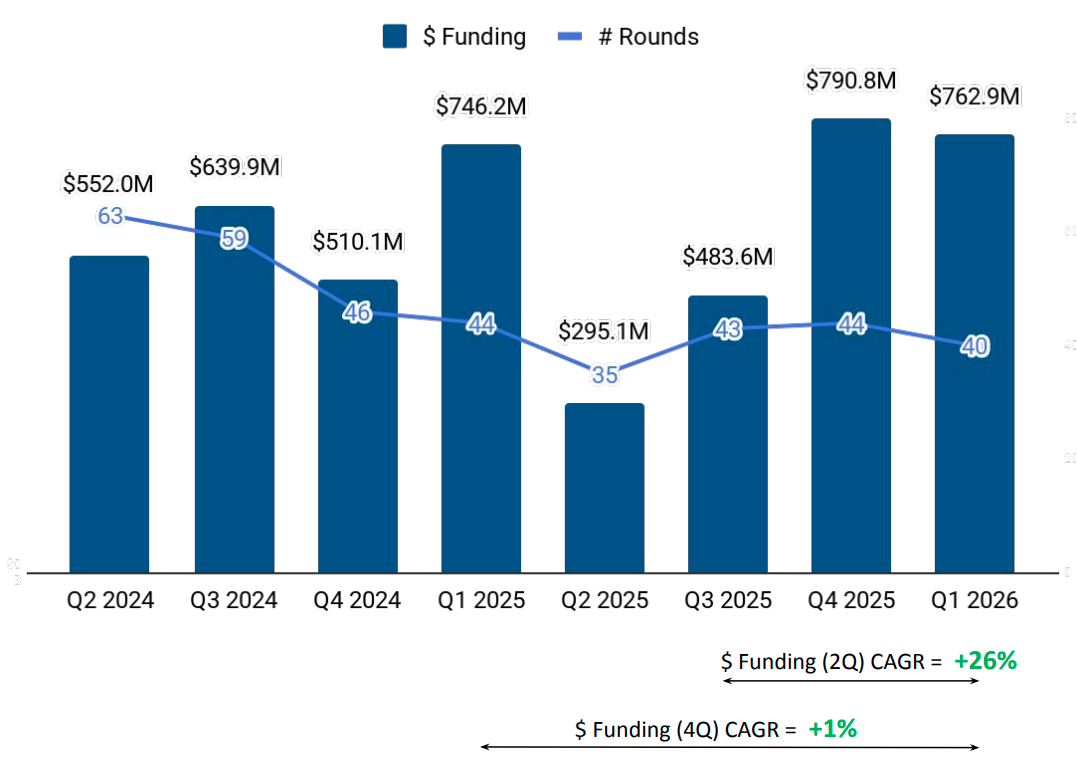

Australia's tech sector opened 2026 on a strong footing, with total equity funding reaching $763M — broadly in line with $746M in Q1 2025. Beneath the stable headline, the quality of capital deployment is rising: two rounds exceeded $100M, late-stage funding stood at $399M compared to $504M in Q1 2025, and the deep-tech and defence pipeline attracted unprecedented capital.

Concentration Over Coverage: The Funding Market Recalibrates

Q1 2026 saw 40 funding rounds — down 9% from 44 in Q1 2025 — yet total funding held steady at $763M versus $746M, meaning the average cheque size grew as investors backed fewer companies with greater conviction. Early-stage funding rose 52% to $323M, reflecting strong appetite for Series A and B companies, while seed deployment grew 34% to $40.9M. Late-stage funding, however, declined 21% to $399M compared to Q1 2025, and first-time-funded companies dropped 50% to just 10 — suggesting that while growth and early-stage capital is flowing confidently, the pipeline at the earliest entry point is one to watch for long-term health.

Startmate, Black Nova, and Exhort Ventures led seed-stage investment activity in Q1 2026, each making two investments in the quarter. At the early stage, OIF Ventures, Co:Act, and Marbruck Investments were the most active, also each closing two deals. Overall, Q1 2026 saw 82 unique institutional investors participate in the Australian tech ecosystem — up from 70 in Q1 2025 — of which 16 were first-time investors, reflecting a healthy influx of new capital alongside continued commitment from established players.

Deep Tech Arrives: Space, Navigation, and Quantum Take the Marquee

The quarter's two standout rounds — Gilmour Space's $145M Series E and Advanced Navigation's $110M Series C — were both in deep technology with dual-use civilian and defence applications, together accounting for nearly a third of all Q1 2026 funding. This reflects a broader sectoral shift: Aerospace, Maritime and Defence Tech attracted $145M in Q1 2026, compared to just $3.1M in Q1 2025, driven by growing national defence strategy, sovereign manufacturing ambition, and rising institutional appetite for dual-use technology.

Quantum hardware also emerged as a notable theme, with Diraq and Silicon Quantum Computing each raising $14M at Series A — collectively deploying $28M into the space in a single quarter. Both are Sydney-based and signal Australia's growing ambition to compete in the global race toward practical quantum computing.

An Exit Market That Is Selective, Not Shut

Q1 2026 recorded 11 acquisitions and zero IPOs, with acquisition activity down 58% from 26 deals in Q1 2025. While the exit market is quieter, the deals that did close demonstrate that appetite for quality Australian assets remains strong. Tyler Tech's $212M acquisition of For the Record was the headline deal, followed by OSL's $58.5M purchase of Banxa and Canva's $20.8M acquisition of Doohly. Notably, Canva — itself an Australian unicorn — featured as an acquirer, a positive sign that the domestic ecosystem is beginning to generate its own strategic consolidators.

Acquirers in Q1 2026 spanned the United States, China, Australia, and Europe, reflecting the global reach of Australian tech assets across software, health tech, fintech, and ad tech. The mix of large disclosed deals alongside several undisclosed-price transactions suggests acquirers are moving selectively but consistently — prioritising strategic fit over volume, and signalling that Australian companies continue to attract serious interest from international buyers.

Geography: Sydney Dominates, but the Map Is Expanding

Sydney led Q1 2026 with 50% of total funding, driven by Advanced Navigation ($110M), Neara ($63.5M), and Lyka ($47.4M), reflecting its strong concentration of mature, later-stage companies. Melbourne followed at 17%, led by AutoGrab ($54.7M) and Applied EV ($40M), both in the vehicle technology space. Gold Coast claimed 19%, powered entirely by Gilmour Space's $145M round — a single deal that highlights how one strategic investment can meaningfully shift a city's funding profile in a given quarter.

Beyond the major cities, Q1 2026 saw encouraging activity from regional hubs, with Adelaide (Splose, $32M), Orange (Cauldron, $13.3M), Newcastle (MGA Thermal, $12.1M), and Wollongong (Sicona, $7M) all recording meaningful rounds. This broadening of the funding map is a positive signal that Australia's tech ecosystem is maturing well beyond its traditional centres.

.svg)