Tracxn has released its UK Climate Tech at a Crossroads: A Funding and Ecosystem Analysis report, providing a data-driven examination of the UK’s climate tech funding landscape, sectoral concentration, demand-side catalysts, and the systemic risks that will define the sector through 2026.

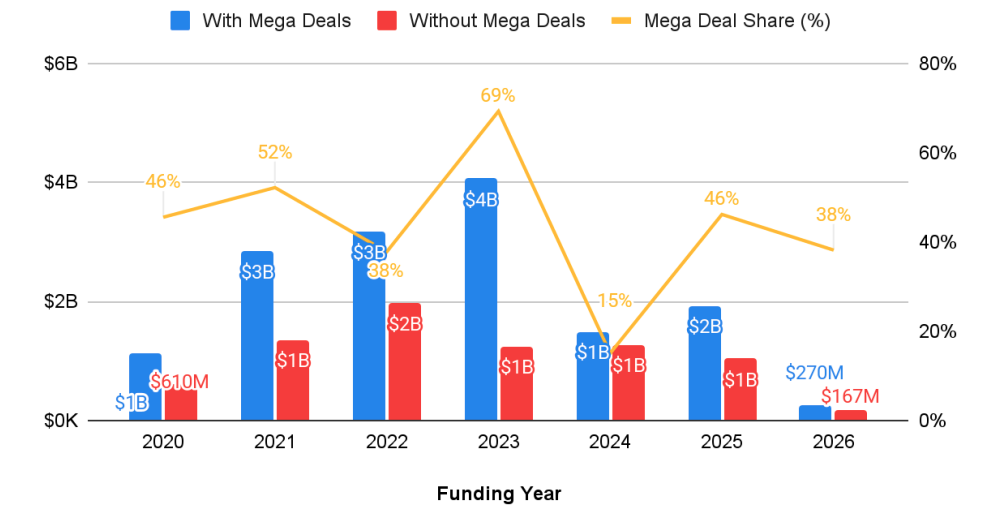

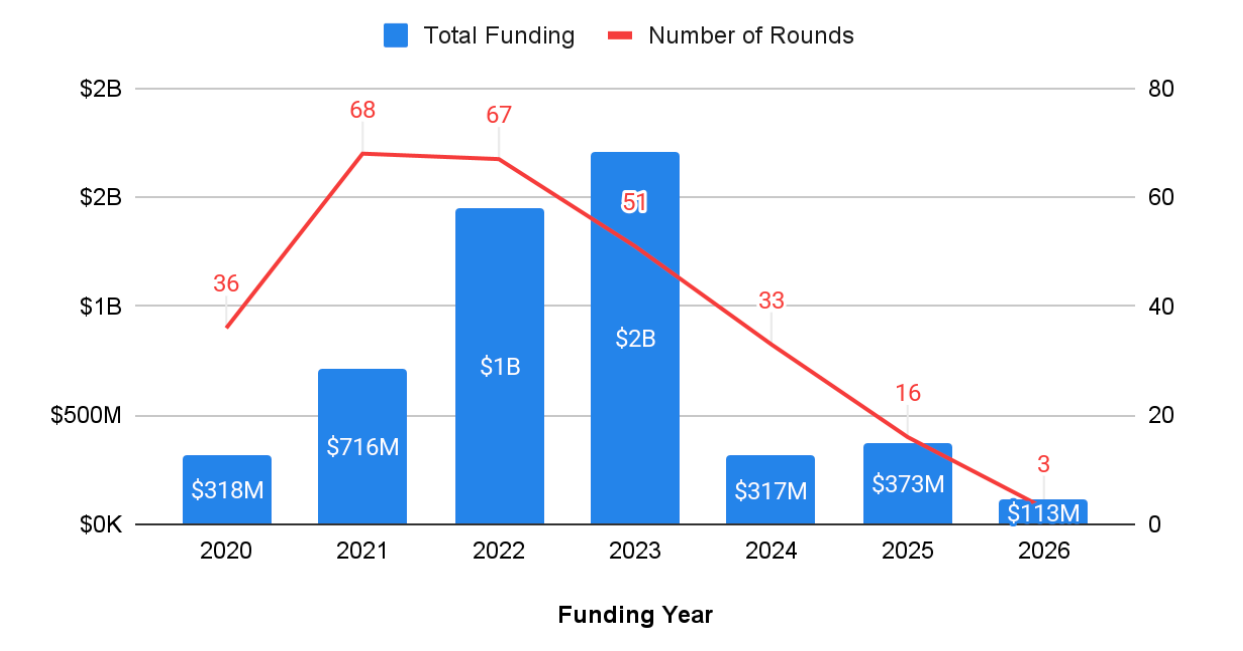

UK climate tech is telling two stories at once. The headline figure, $1.9B raised in 2025, down from a $3.8B peak in 2023 suggests a sector in retreat. But almost all of that drop is explained by fewer mega-deals ($100M+ rounds), not a collapse in ordinary funding activity. In 2023, mega-deals made up 69% of total funding; in 2025, just 38%. Strip those large cheques out, and the underlying ecosystem has raised roughly $1B every year since 2021, with the median deal size growing from $968K in 2020 to $3M in 2024. By that measure, the true ecosystem peak was not 2023 but 2022, when $2B was deployed across 310 rounds, a broader, deeper market than any headline year since.

Where capital has flowed, it has concentrated in the infrastructure underpinning the UK’s electrification push. Smart grid leads at $3.4B in cumulative funding, followed by air pollution management ($1.5B), renewable energy tech ($1.3B), energy efficiency ($1.2B), and solid waste management ($730M). The top three companies are Octopus Energy, Zenobē, and Fidra Energy together embody the infrastructure, power supply, and hardware stack required for a zero-emission grid. Policy backing is substantive: Ofgem approved over £28B of energy infrastructure investment in December 2025. Yet deployment remains constrained, with NESO unable to meet connection deadlines for 210 of 340 protected projects.

The emerging catalyst is AI-driven power demand. The IEA’s base case projects global data centre electricity consumption more than doubling from ~415 TWh in 2024 to ~945 TWh by 2030, approaching 3% of global electricity. UK AI funding reached $4.6B in Q1 2026, with neocloud Nscale alone raising $2.0B. OpenAI’s decision to pause its UK Stargate data centre project citing high energy prices and regulatory friction illustrates how clean power has become a prerequisite for AI competitiveness rather than an adjacent concern.

Converting this inflection into scaled deployment will depend on three policy levers. First, energy security through diversification with US–Iran tensions redefining the energy landscape, climate tech serves as both deterrent against and immunity from shocks, and funding cannot be allowed to redirect toward fossil fuels. Second, sustained government incentives: China’s targeted EV subsidies proved the model works, and the UK government’s recent £380M grant to Tata’s Somerset battery factory is the right signal. Third, supportive immigration policy to close the engineering shortage, Northvolt’s bankruptcy showed how talent gaps can sink otherwise well-funded companies, and skilled-talent inflow remains the single fastest lever available.

Three principal risks could still constrain the inflection. An AI market correction would cascade across climate tech given its growing dependence on hyperscaler power demand. Immigration policy constraints remain the binding people-side bottleneck. Smart grid, the most-funded sector, is precisely where the UK engineering shortage is most acute. Physical grid capacity continues to limit deployment regardless of funding availability. On the eve of Earth Day 2026, the conversation is shifting from emissions rhetoric to the economics of energy, infrastructure, and industrial competitiveness, the structural signal to watch for the remainder of 2026.

.svg)