Tracxn has released its latest report on the United States Tech ecosystem for Q1 2026, highlighting a significant surge in funding activity alongside notable shifts across sectors, stages, and deal activity. United States is the highest funded country in Q1 2026 ahead of United Kingdom and China at positions 3rd and 4th respectively. The quarter reflects strong capital inflow driven by large funding rounds and sectoral momentum.

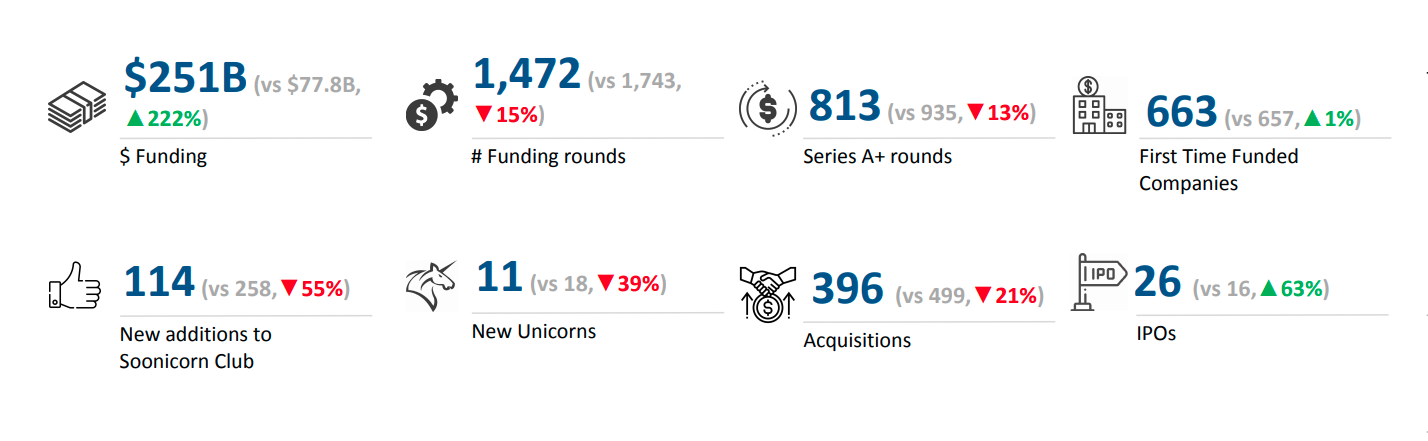

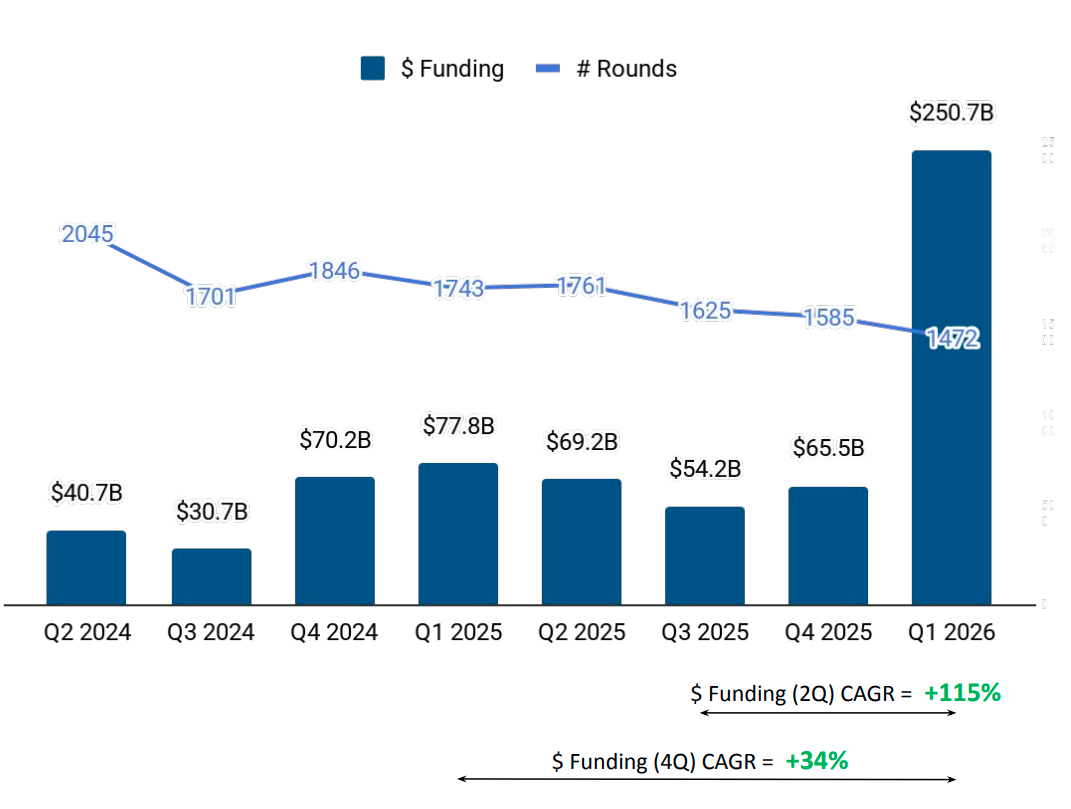

A total of $251B was raised in Q1 2026, a rise of 283% compared to $65.5B raised in Q4 2025, and a rise of 222% compared to $77.8B raised in Q1 2025. This sharp increase in funding highlights a substantial expansion in capital deployment compared to both the previous quarter and the same period last year.

Seed Stage saw a total funding of $3.2B in Q1 2026, a rise of 9% compared to $3.0B raised in Q4 2025, and a rise of 35% compared to $2.4B raised in Q1 2025. Early Stage saw a total funding of $20.8B in Q1 2026, a drop of 1% compared to $20.9B raised in Q4 2025, and a rise of 59% compared to $13.0B raised in Q1 2025. Late Stage saw a total funding of $227B in Q1 2026, a rise of 445% compared to $41.6B raised in Q4 2025, and a rise of 263% compared to $62.4B raised in Q1 2025.

Enterprise Applications, Transportation and Logistics Tech, & Life Sciences were the top-performing sectors in Q1 2026 in this space. Enterprise Applications sector saw a total funding of $207B in Q1 2026 which is an increase of 379% when compared to $43.3B raised in Q4 2025 and an increase of 224% when compared to $63.9B raised in Q1 2025. Transportation and Logistics Tech sector saw a total funding of $18.2B in Q1 2026 which is an increase of 1553% when compared to $1.1B raised in Q4 2025 and an increase of 1220% when compared to $1.4B raised in Q1 2025. Life Sciences sector saw a total funding of $8.4B in Q1 2026 which is an increase of 28% when compared to $6.6B raised in Q4 2025 and an increase of 25% when compared to $6.7B raised in Q1 2025.

Q1 2026 has witnessed 10 mega funding rounds when compared to 9 such rounds in Q4 2025 and 3 such rounds in Q1 2025. Companies like OpenAI, Anthropic, and xAI have managed to raise mega funding rounds in this period. OpenAI has raised a total of $122B in a Series G round. Anthropic has raised a total of $40B in funding across its Series F and Series G rounds. xAI has raised a total of $20B in a Series E round. A major part of these mega funding rounds are from Enterprise Applications, Transportation and Logistics Tech, & Aerospace, Maritime and Defense Tech.

US Tech recorded 26 IPOs in Q1 2026, up 24% from 21 in Q4 2025, and up by 63% from 16 in Q1 2025. MiniMed, EquipmentShare and York Space Systems are some of the companies that went public in Q1 2026. There were 11 unicorns created in Q1 2026, and a drop of 39% compared to 18 in Q4 2025, and in Q1 2025.

Tech companies in United States saw 396 acquisitions in Q1 2026, which is a drop of 4% as compared to 411 acquisitions in Q4 2025 and a drop of 21% compared to 499 acquisitions in Q1 2025. Exact Sciences was acquired by Abbott at a price of $21B, becoming the highest valued acquisition in Q1 2026. This was followed by the acquisition of Masimo acquired by Danaher at a price of $9.9B.

San Francisco led the United States tech funding landscape in Q1 2026, accounting for 68% of the total capital raised by tech companies, reflecting a strong concentration of investment activity in the city and reinforcing its dominance in the ecosystem, while Palo Alto followed as a distant second, contributing 9% of the overall funding.

Y Combinator, Andreessen Horowitz, and General Catalyst were the top seed stage investors in US Tech ecosystem for Q1 2026. Sequoia Capital, Lightspeed Venture Partners, and Accel were the top early stage investors in US Tech ecosystem for Q1 2026. 1789 Capital, DST Global and Woven Capital were the top late stage investors in US Tech ecosystem for Q1 2026.

The United States tech ecosystem witnessed a significant surge in Q1 2026, with total funding reaching $251B driven largely by late-stage investments and mega funding rounds. The dominance of Enterprise Applications, Transportation and Logistics Tech, & Life Sciences sectors underscores strong capital concentration in key industries. While early-stage funding remained relatively stable and seed-stage funding saw moderate growth, the sharp rise in late-stage investments played a central role in overall funding expansion.

.svg)